Dangerous Cocktail

An energy shock, fragile creditors, and rising yields are beginning to mix into something dangerous.

Speaking from the White House briefing room on Easter Monday, President Donald Trump shifted his rhetoric to Pacific nations, having previously directed sharp criticism at NATO members:

“You know who else didn’t help us? South Korea didn’t help us. You know who else didn’t help us? Australia didn’t help us. You know who else didn’t help us? Japan.

We’ve got 50,000 soldiers in Japan to protect them from North Korea. We have 45,000 soldiers in South Korea to protect us from Kim Jong Un, who I get along with very well.”

Although the figures may be overstated, Trump does have a point: the U.S. still provides these countries with a meaningful security umbrella. But for Japan, South Korea, and many others, energy security is a far more immediate and pressing concern.

Washington may be tempted to see this as someone else’s problem. After all, Japan and South Korea did little to help the U.S. reopen the Strait of Hormuz, while the United States itself imports relatively little oil through the chokepoint and often presents itself as energy independent. But that view misses a more important reality: the global energy market is deeply intertwined with the U.S. bond market, and the bond market remains the foundation of American financial power.

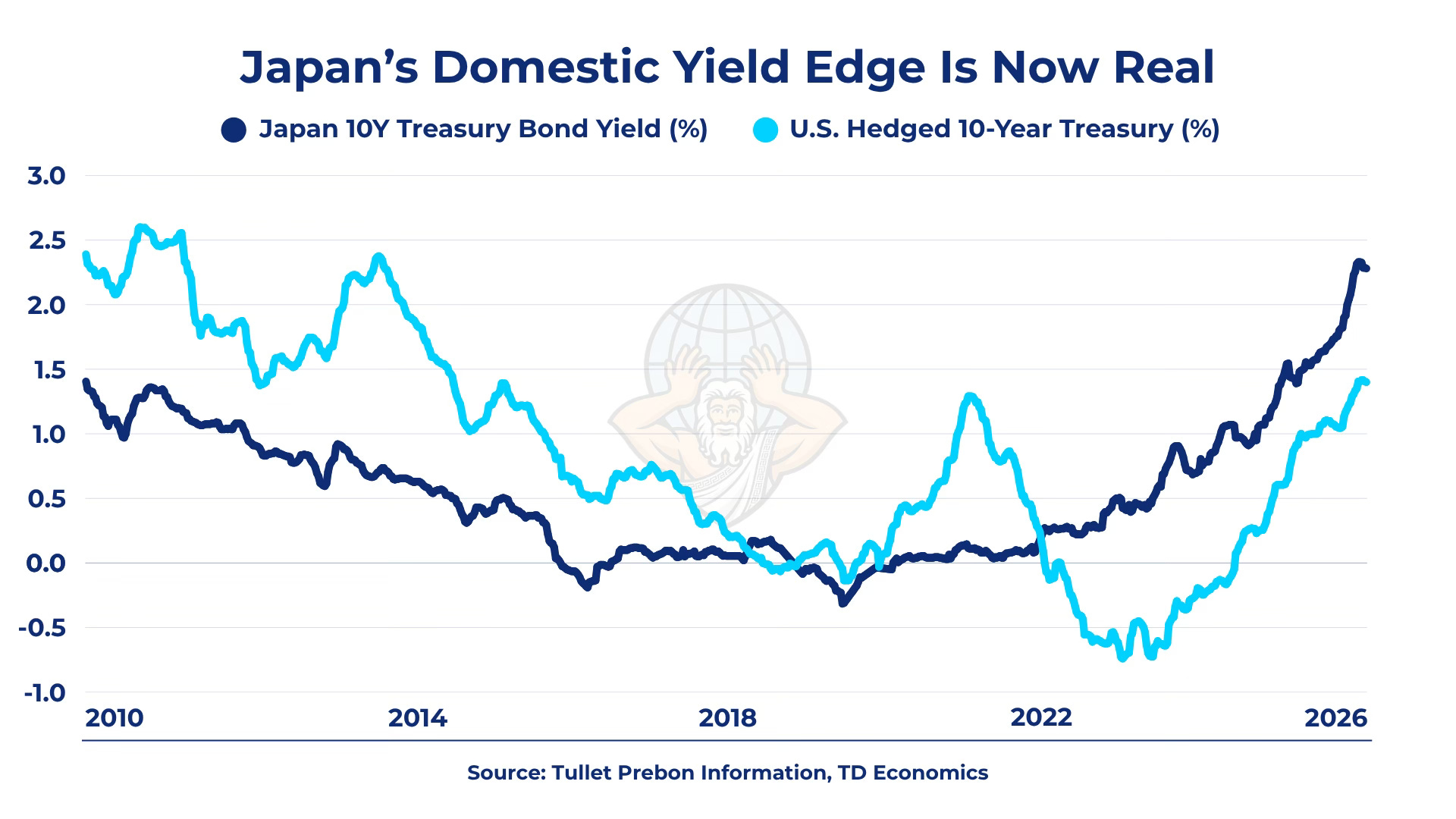

Japan has become the canary in the coal mine for this dynamic. It is the most important marginal buyer of newly issued U.S. Treasuries, holding roughly $1.2 trillion in U.S. government debt and ranking as the largest foreign creditor to Washington. But that role is no longer guaranteed. As energy costs surge and Japan’s monetary landscape begins to shift, even Washington’s most loyal creditor may be forced to rethink its exposure.

Japan imports roughly 95% of its oil from the Middle East, along with around 11% of its liquefied natural gas. Of those supplies, approximately 70% of its oil and 6% of its LNG pass through the Strait of Hormuz, a chokepoint that has now been effectively closed for more than a month. This forces Asian refiners in countries like Japan to pay record-high premiums for Non-Middle East Crude.

This energy shock is hitting Japan at an especially fragile moment. With the Bank of Japan still leaning toward further tightening, the 10-year JGB yield has risen to roughly 2.4%, near multi-decade highs. At the same time, imported energy costs are feeding inflation and worsening domestic financial conditions. The result is a dangerous shift in incentives: Japanese capital now has more reason to stay home, and less reason to keep underwriting the U.S. Treasury market at the margin.

That shift matters because America’s military system is not financed in isolation. It is funded through a bond market that depends on surplus economies remaining liquid, stable, and willing to recycle capital into Washington. But those same economies are now being squeezed by the energy disorder surrounding U.S. power projection itself.

What follows from that shift is not abstract. If Japan begins to scale back its purchases—or worse, starts liquidating holdings to pay for energy bills—the effects would be felt immediately in the one market Washington can least afford to destabilize.

At the margin, fewer foreign buyers mean higher yields. And in a system already strained by elevated debt levels and persistent issuance, that marginal shift carries disproportionate weight. The United States can no longer rely on price-insensitive absorption—allies who buy bonds regardless of cost—to fund deficits nearing $2 trillion annually.

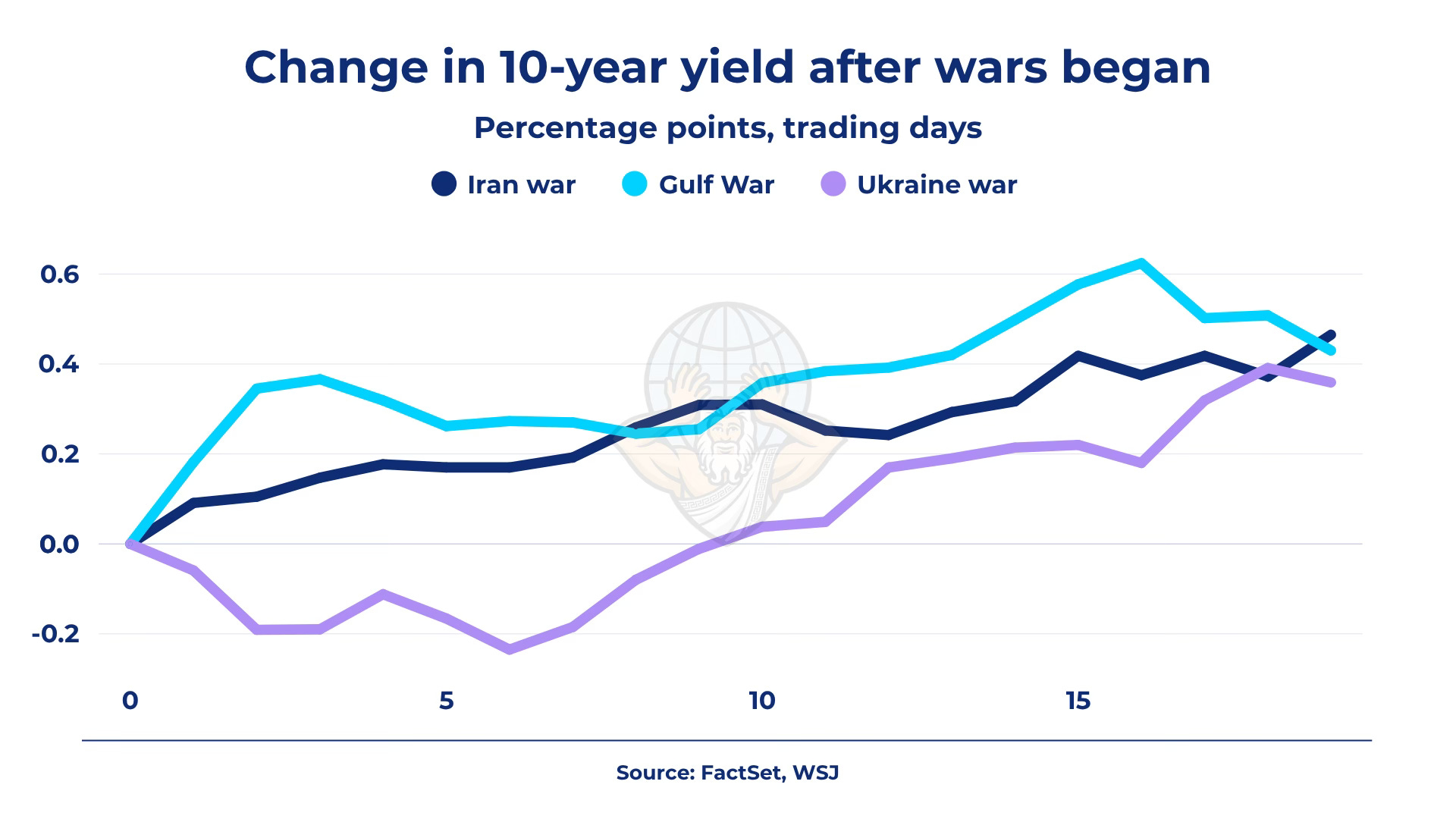

The historical comparison is telling. In the early trading sessions after this conflict began, the U.S. 10-year yield has behaved far less like it did after the outbreak of the Ukraine war—where yields initially dipped as investors sought a flight to safety—and far more like the early Gulf War pattern.

During the Ukraine crisis, yields dropped nearly 0.25 percentage points in the first week. This time, however, they are rising instead, echoing the Gulf War trajectory in which markets quickly began pricing inflation, supply risk, and fiscal strain. If even war no longer produces a reliable bid for Treasuries, Washington is no longer confronting ordinary volatility. It is confronting the possibility that the financial logic underpinning its power is beginning to change.

There is precedent for this—and with some irony, it passed through the very same canal. In 1956, Britain marched into Suez believing it still possessed the reflexes of empire. What it lacked was the balance sheet. Sterling came under pressure, reserves drained, and London was forced to seek emergency dollar support from Washington and the IMF. The support that came with a condition: withdraw. Britain’s retreat from Suez was not dictated by military weakness, but by financial vulnerability. Great powers rarely discover their limits when they run out of weapons. More often, they discover them when funding begins to fail.

Washington now risks running into a similar constraint. In a wartime environment, its dependence on continuous, price-insensitive demand for debt becomes even more acute. Rising yields would tighten financial conditions precisely as fiscal outlays expand, forcing the United States into an increasingly narrow corridor: either absorb higher borrowing costs and the slowdown that follows, or lean more heavily on domestic balance sheets and central bank support.

In other words, what begins as an energy shock in Asia does not stay there. It feeds back into the U.S. funding market—and from there, into the core of the global financial system. Japan serves as the primary example, but the trend is broader: the top three holders of U.S. Treasuries are all becoming increasingly unreliable sources of steady demand.

China has already been quietly stepping back from the U.S. Treasury market for years, even urging banks to curb exposure. The United Kingdom surpassed it as the second-largest foreign holder in March last year, but that should not be mistaken for a sign of greater stability.

The UK is no longer the energy-secure creditor it once was. It now imports roughly 44% of its energy, a sharp reversal from the 1980s and 1990s when it was a net exporter. This means that yet another pillar of the U.S. debt market is now dangerously exposed to the same global energy shocks that are currently rippling through the system. Together, Japan, China, and the UK account for roughly 30% of all foreign-held U.S. Treasuries.

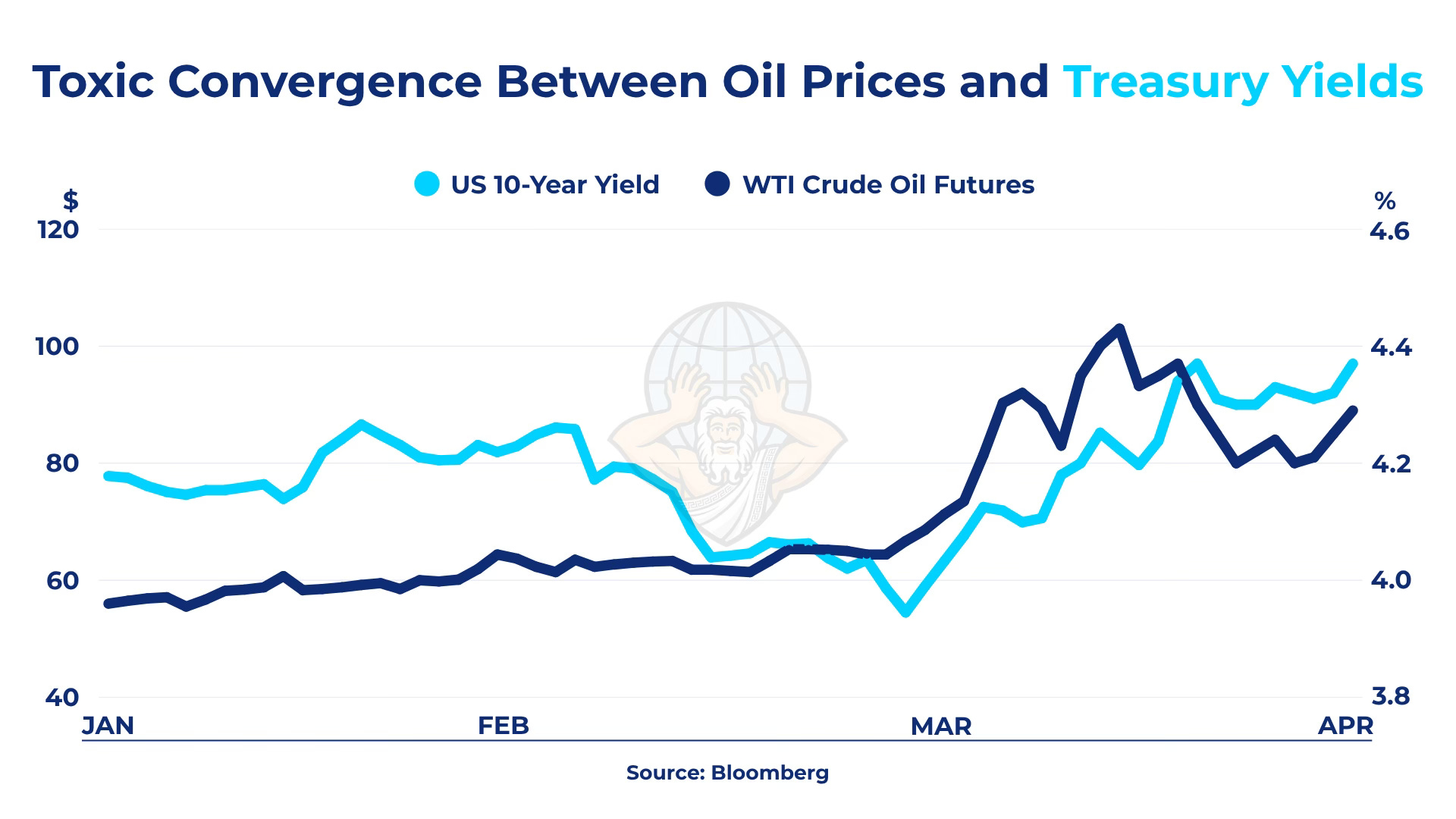

This is the chilling reality Washington is beginning to run into. Political rhetoric often treats war as a test of national resolve. Financial markets treat it as a matter of solvency. The old decoupling between energy prices and bond yields is breaking down. WTI crude and the U.S. 10-year yield are increasingly moving in the same direction, a dangerous signal.

That correlation should bury the fantasy of energy-independent American power. Oil is no longer just a driver of domestic inflation; it is increasingly a source of pressure on the very creditor system that helps finance American deficits.

For Japan, the calculus is brutal. As an economy forced to choose between keeping its lights on and financing the American deficit, it will choose the former every time. If this war drags on, liquidation of U.S. Treasuries becomes less a choice than a necessity—an unavoidable consequence of funding record-high energy costs in a world where the Strait of Hormuz has become a graveyard for global trade.

Therefore, the United States cannot afford a long war. It lacks the fiscal cushion, it lacks the foreign bid, and it lacks the luxury of time. If the 10-year yield continues to track the upward surge of oil prices, it will inevitably cross thresholds that head into territory that would effectively freeze the American housing market and paralyze domestic consumption.

Washington was never prepared for a world in which its military ambitions would be financed by creditors whose own stability depends on the very energy prices those ambitions are destabilizing.

If this shock persists, the contradiction at the center of American power becomes impossible to ignore. Washington’s security umbrella is being financed by creditors whose own stability depends on the energy flows now being thrown into disorder.

The system still functions, but the logic holding it together is beginning to fail. And once America’s creditors are forced to choose between funding Washington and funding themselves, the choice will not be difficult.

Subscribe to receive my posts directly in your inbox and support my work!

Share this with anyone if you think their attention span can survive more than two paragraphs — and if not, send it anyway. 📨

The world has changed.

Bond market?

The 90s are over and Uber War only has 1 client 🇺🇸.

Trump isn’t Clinton, the Bushes or Obama.

Enlightening essay—thank you. Godspeed