Fault Lines

The semiconductor order is being rebuilt around geopolitical durability

For decades, the global semiconductor system rested on a dangerous assumption: that Taiwan’s centrality made war irrational. The logic was elegant. If the world’s most advanced chips were concentrated on one island sitting barely 180 kilometers from mainland China, then no serious actor would risk disrupting it.

The economic consequences would simply be too catastrophic. Smartphones, data centers, military systems, cloud infrastructure, financial networks, industrial automation, automobiles, telecommunications, artificial intelligence. Much of the most advanced layer of that system flowed, directly or indirectly, through Taiwan Semiconductor Manufacturing Company (TSMC). Concentration itself became deterrence.

This came to be known as the Silicon Shield. But embedded inside that framework was a deeper assumption that only functioned in a specific era of globalization: that interdependence would always stabilize geopolitical competition rather than intensify it.

That assumption is beginning to break down. Every new advanced fabrication plant built in Arizona quietly changes the strategic meaning of Taiwan. Every additional semiconductor subsidy routed into Intel, TSMC, Samsung, or domestic packaging infrastructure reflects the same realization in Washington: the United States no longer wants the modern economy dependent on a single island increasingly exposed to Chinese military pressure. The semiconductor race is no longer primarily about technological leadership. It is becoming a contest over which system can survive fragmentation.

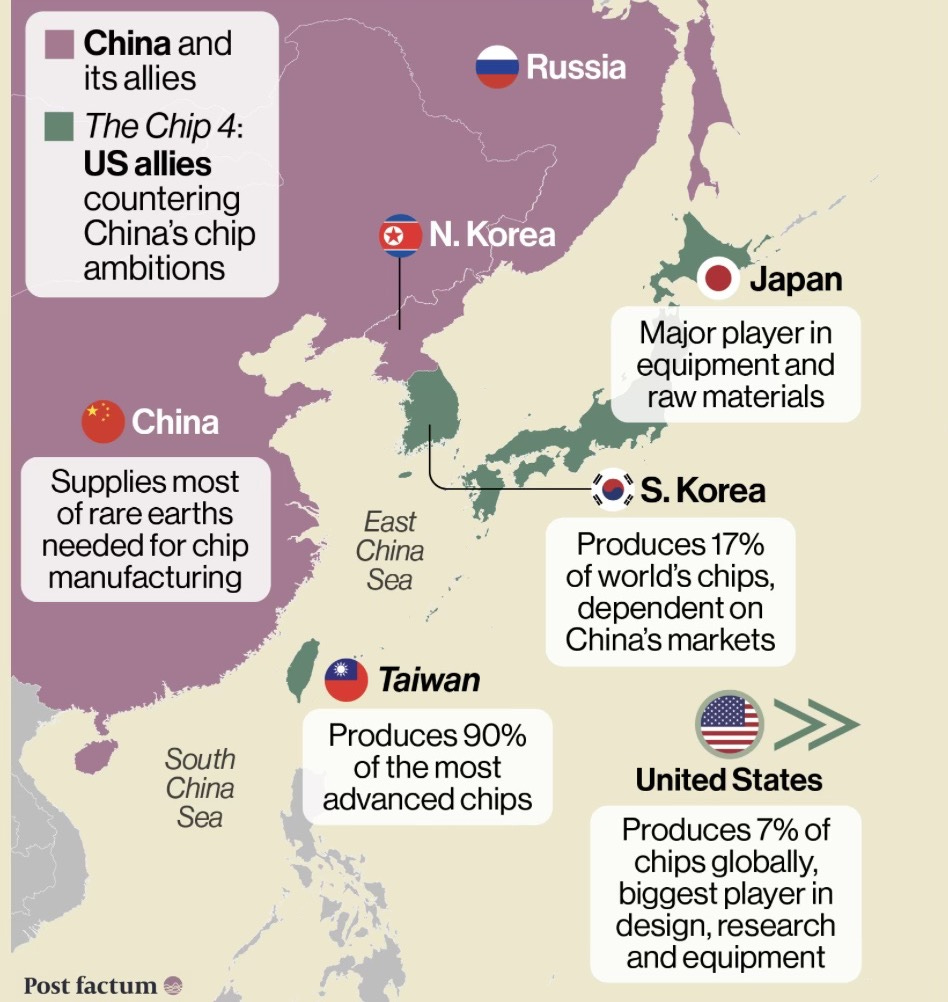

The semiconductor industry itself evolved through extreme specialization. The United States retained dominance in chip design software, processor architecture, and intellectual property, while Taiwan became the world’s dominant hub for advanced foundry manufacturing. Japan specialized in chemicals, wafers, and precision materials. The Netherlands became indispensable through ASML’s monopoly on extreme ultraviolet lithography systems. South Korea dominated memory chips. Southeast Asia absorbed packaging and assembly.

The production of a single advanced chip now requires more than 500 stages spread across multiple jurisdictions, with components and materials often traveling over 25,000 miles before final integration.

That complexity created extraordinary efficiency, but also extraordinary fragility. By the late 2010s, East Asia accounted for more than 80% of global semiconductor fabrication capacity, while Taiwan and South Korea alone represented roughly 45% of global production. TSMC itself grew into something historically unprecedented. By 2023, the company controlled around 60% of the global foundry market and over 90% of advanced chips below 10 nanometers. At the frontier, the industry effectively condensed into one island.

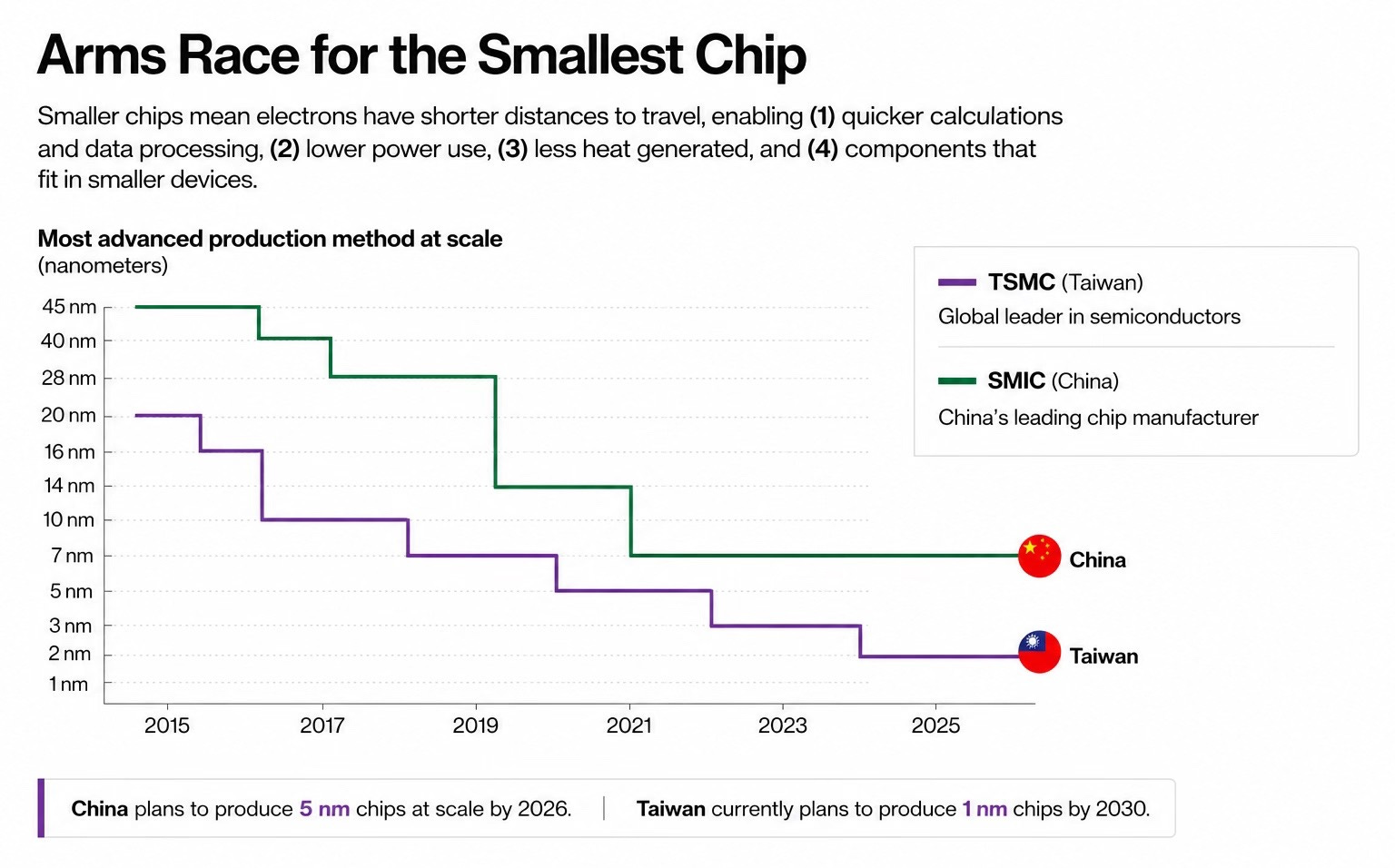

This concentration became even more important once artificial intelligence entered the equation. Smaller nodes are not simply marketing language. The difference between 7nm, 5nm, 3nm, and eventually 2nm chips determines transistor density, heat generation, power efficiency, and computational speed. Smaller transistors allow electrons to travel shorter distances, improving processing capability while reducing energy consumption.

That matters enormously for AI clusters, military systems, cloud infrastructure, and advanced weapons. Taiwan currently dominates this frontier while China’s SMIC —its largest and most advanced chipmaker— remains materially behind, despite rapid progress under sanctions pressure.

Yet the strategic picture is more complicated than many Western narratives suggest. Much of the discussion around semiconductors focuses almost entirely on cutting-edge AI processors, Nvidia GPUs, or export controls around advanced lithography. But modern industrial civilization does not run purely on frontier chips. Mature-node semiconductors remain foundational to automobiles, electrical grids, telecom systems, industrial automation, robotics, drones, sensors, and missile systems.

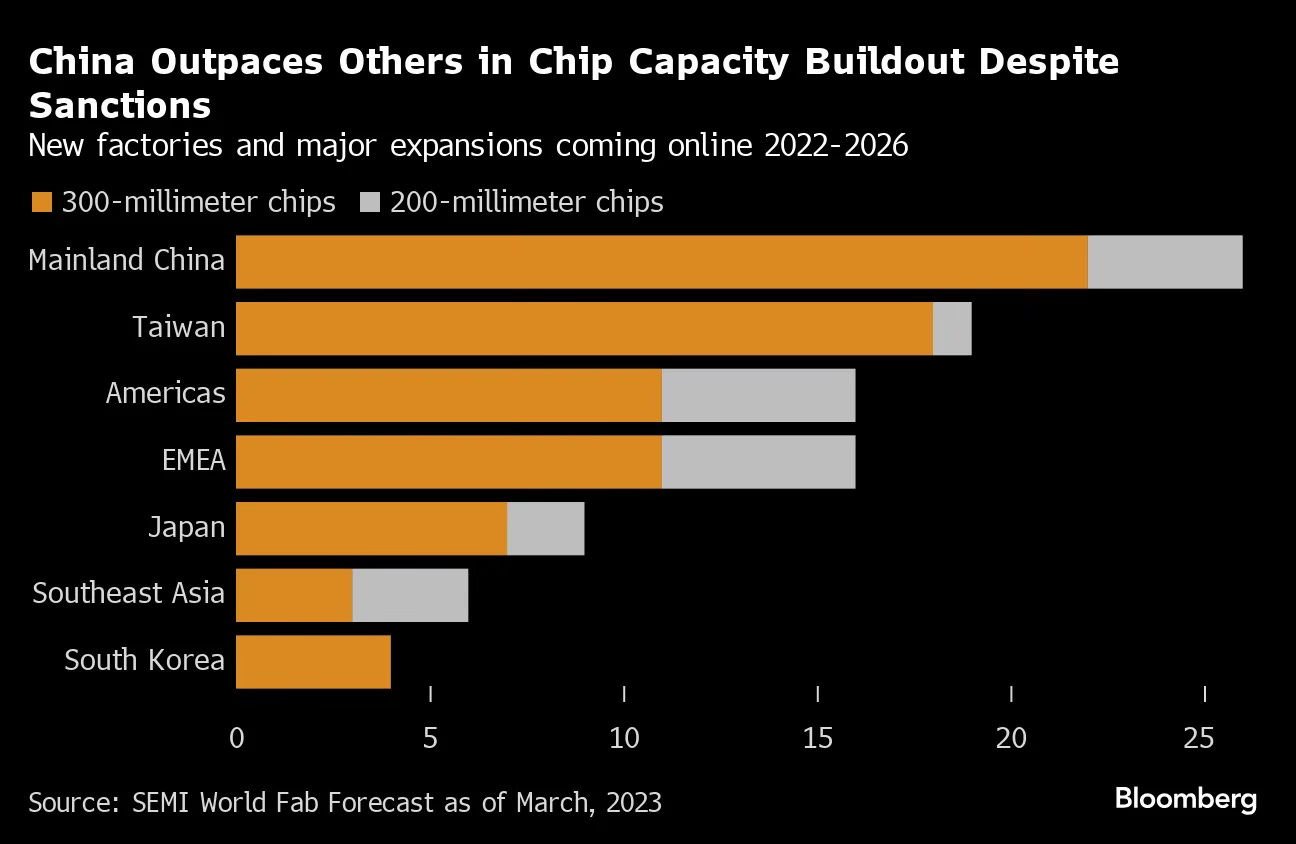

China is now constructing more semiconductor facilities than any other region between 2022 and 2026 despite sanctions pressure. The chart itself is revealing. Mainland China significantly outpaces the Americas, Japan, Europe, and South Korea in total fab expansion, especially in 300-millimeter industrial-scale wafer production.

This reflects a very different strategic logic than the one dominating Silicon Valley narratives. The West became obsessed with frontier AI acceleration. China increasingly appears focused on industrial endurance. That distinction matters because tech wars are rarely won solely by whoever possesses the most advanced prototype. They are often won by whoever maintains industrial continuity longest under stress.

Beijing’s semiconductor strategy increasingly resembles a wartime industrial architecture rather than a purely commercial one. Electric vehicles provide a good example. China is already the world’s largest EV market, and EV production requires enormous quantities of semiconductors for braking systems, sensors, power management, battery systems, and onboard computing. Scaling domestic semiconductor depth in these sectors reduces external vulnerability while simultaneously strengthening broader industrial autonomy.

Even if China remains behind at the most advanced nodes, it may still achieve something strategically sufficient: the ability to sustain industrial and military functionality under prolonged technological confrontation.

This is precisely why Intel matters again.

For years, markets viewed Intel through the lens of quarterly earnings, lost market share, delays, and failed execution against rivals like TSMC and Nvidia. But that framing increasingly misses the larger shift underway. Intel is no longer functioning solely as a commercial semiconductor company. It is becoming a national absorption mechanism for frontier manufacturing risk.

The economics of advanced fabrication have become almost absurd. High-NA EUV systems produced by ASML cost hundreds of millions of dollars per unit before installation. Entire facilities must be redesigned around vibration tolerance, airflow management, thermal stability, and power delivery. Yield problems can persist for years. The frontier itself has become physically expensive in ways software investors struggle to fully appreciate. At a certain point, the private market alone becomes structurally incapable of carrying the risk.

This is where the CHIPS Act fundamentally altered the semiconductor landscape. Public discussion framed it as industrial policy or subsidies, but in practice it represented something more important: the partial militarization of semiconductor manufacturing capacity. Once Washington concluded that advanced logic manufacturing could not be allowed to disappear domestically, profitability stopped being the only relevant metric.

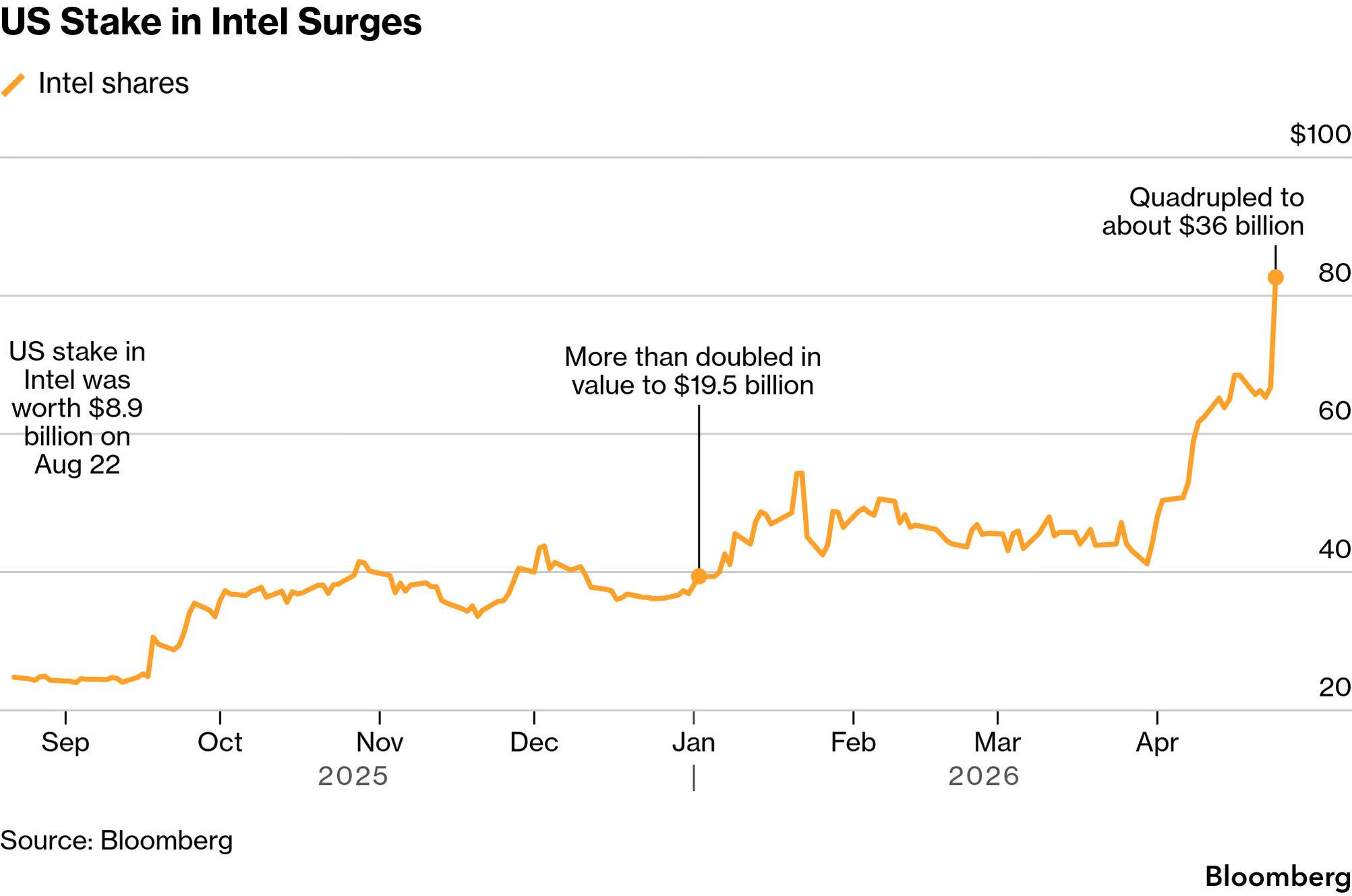

The U.S. government’s Intel position reveals how far this transition has already advanced. Bloomberg reported that the White House agreement would ultimately leave the U.S. taxpayer owning roughly 433 million Intel shares, initially valued around $8.9 billion before surging toward approximately $36 billion as Intel stock rallied.

Following the Bloomberg report, the stock rallied another 50% hitting new all-time-high. Markets interpreted this primarily as a successful investment. Strategically, it looks more like something else entirely: the state anchoring domestic semiconductor survivability directly onto the national balance sheet.

That distinction matters enormously. Governments do not absorb billions in exposure to struggling industrial firms unless the underlying capability is viewed as systemically necessary. Intel’s importance no longer sits purely inside quarterly earnings. It sits inside the reality that no serious superpower wants to remain entirely dependent on offshore frontier manufacturing located within missile range of a geopolitical rival. In an interview last week, President Donald Trump did not mince words:

“We were the car capital of the world 50 or 60 years ago, and then they just started taking them away. We were the chip capital of the world and now -- you know, Intel -- and now they're coming back, all the chip companies are coming back. You might say a word about that, Howard, real fast, because we are -- what we're doing with chips is incredible.”

Washington increasingly appears willing to tolerate inefficiency, duplication, and enormous capital intensity in exchange for geographic redundancy. The logic resembles Cold War infrastructure more than modern shareholder capitalism. Semiconductor fabs are slowly being reclassified from commercial assets into strategic industrial nodes.

TSMC’s expansion into the United States reflects the same shift from a different angle. The company’s decision to commit $165 billion toward American semiconductor manufacturing fabs in Arizona was not simply an investment announcement. It was a geopolitical signal. Washington is no longer content merely protecting Taiwan’s fabs through military deterrence. It is geographically internalizing portions of the semiconductor supply chain itself.

This matters enormously because it changes the underlying logic of the Silicon Shield. Taiwan’s original strategic value rested on concentration. The island became indispensable precisely because so much advanced production remained physically trapped there. But the more semiconductor capability migrates toward Arizona, Oregon, Japan, Germany, and other allied jurisdictions, the more the global system becomes capable of surviving instability around Taiwan itself.

Taipei and Washington increasingly have overlapping but not identical objectives. Taiwan wants indispensability. The United States wants resilience. Those are not necessarily the same thing.

This does not mean Washington is abandoning Taiwan. Quite the opposite. American military cooperation with Taipei continues to deepen while Chinese military activity around the island intensifies. But beneath the visible headlines, something more structural is occurring. The United States appears to be preparing for a world in which semiconductor concentration itself has become strategically unacceptable.

At the same time, the limits of reshoring are becoming increasingly visible. The United States still depends entirely on ASML for EUV lithography systems, with no domestic alternative in development. Advanced packaging remains overwhelmingly concentrated in Asia. TSMC’s Arizona expansion has already encountered delays, labor shortages, cost overruns, and operational challenges. Manufacturing advanced semiconductors in the United States can cost 30% to 50% more than in Asia due to labor, regulatory, and supply chain disadvantages.

That means Washington is not pursuing true self-sufficiency. It is pursuing allied redundancy.

The Chip 4 framework increasingly reflects this reality. The United States contributes design software and system architecture. Japan anchors materials and tooling. South Korea dominates memory production. Taiwan remains central to leading-edge foundries. Rather than rebuilding the entire stack domestically, Washington appears to be constructing a bloc-based semiconductor architecture designed to survive geopolitical fracture.

China appears to understand this transition as well. In April, Xi Jinping met with Taiwan opposition leader Cheng Li-wun in a rare high-level encounter that immediately generated controversy inside Taiwan. Xi declared that people on both sides of the Taiwan Strait were Chinese and wanted peace, while Cheng argued Taiwan should become “a symbol of peace jointly safeguarded by Chinese people on both sides of the strait.” Viewed superficially, the meeting looked symbolic. Strategically, it revealed something deeper.

China is no longer relying solely on military pressure around Taiwan. It is simultaneously applying political pressure, economic pressure, psychological pressure, and industrial pressure. Taiwan itself is increasingly divided over how confrontation with Beijing should be managed. While the ruling Democratic Progressive Party continues emphasizing sovereignty and military preparedness, opposition factions argue that deteriorating cross-strait relations increase risk rather than security.

This internal fragmentation matters because the semiconductor system was built during a period when the political foundations underneath globalization were assumed to be relatively stable. They no longer are. China’s military exercises increasingly resemble rehearsals for economic strangulation rather than outright invasion. Large-scale blockade drills, cyber pressure, gray-zone coercion, and maritime disruption all exploit the same reality: Taiwan’s semiconductor centrality creates leverage for both sides.

But here again, the strategic meaning changes if semiconductor concentration itself begins dispersing outward.

This is the paradox quietly emerging beneath the semiconductor race. The United States is strengthening Taiwan militarily while simultaneously reducing systemic dependence on Taiwan economically. China is increasing pressure on Taiwan while simultaneously attempting to reduce dependence on Western semiconductor systems industrially. Both powers increasingly appear to be preparing for a world where interdependence becomes less stabilizing and more weaponized.

The irony is that the original Silicon Shield may have succeeded too well. Taiwan became so important that the risks associated with concentration eventually became intolerable for the very system that created it. Arizona fabs are not replacing Taiwan. Intel is not replacing TSMC. Japan is not replacing Silicon Valley. The system is evolving into something more geographically distributed, politically aligned, and strategically redundant.

In effect, the semiconductor order is becoming bloc-based. The globalization era optimized for efficiency. The fragmentation era optimizes for survivability. Markets still tend to interpret semiconductor developments through a commercial lens: AI demand, earnings reports, GPU shortages, export controls, valuation multiples. Those variables matter, but they increasingly sit downstream from something larger.

The semiconductor system is quietly being reorganized around geopolitical durability. What began as a supply chain is becoming security architecture. The most important semiconductor transition underway today is not technological. It is geographical. And geography, once it re-enters the system, rarely leaves quietly.

That is also why this week’s summit between Xi Jinping and Donald Trump matters far beyond trade headlines alone. Beneath the optics sits a deeper question: whether the world’s most strategic industry will remain interconnected, or continue hardening into competing technological spheres.

Subscribe to receive my posts directly in your inbox and support my work!

Share this with anyone if you think their attention span can survive more than two paragraphs — and if not, send it anyway. 📨

Brilliant piece of insight writing by Atlas. Touching upon the complexities of the geopolitical realities. A must read. Looking forward to more and deeper reviews of a world in transition.

I’ve been watching this evolution too. It appears that China and the US have come to an understanding. Eventually, China will take Taiwan. China has provided fair warning of something that the US could not prevent, and by doing so, has allowed the Americans to make the appropriate investment adjustments. If we didn’t have access to the latest chip technology, we would be forced to defend Taiwan, which would be a disaster.

I suspect that this ‘deal’ will keep the two superpowers from engaging militarily. As soon as TSMC technology and fabrication is established in the US, China will have the green light to do what they will do.