Ground Shifts

How control over Kazakh uranium shifted from ownership to infrastructure—and left the U.S. outside

Kazakhstan’s latest move in its uranium sector is being sold as technocratic reform. It isn’t.

The December amendments to the Subsoil Use Code mark a deliberate consolidation of state power over one of the most strategically sensitive commodities on earth. By granting Kazatomprom priority access to new deposits, tightening renewal terms on existing licenses, and pushing majority ownership thresholds toward 90%, Astana is not liberalizing its energy future. It is hardening it.

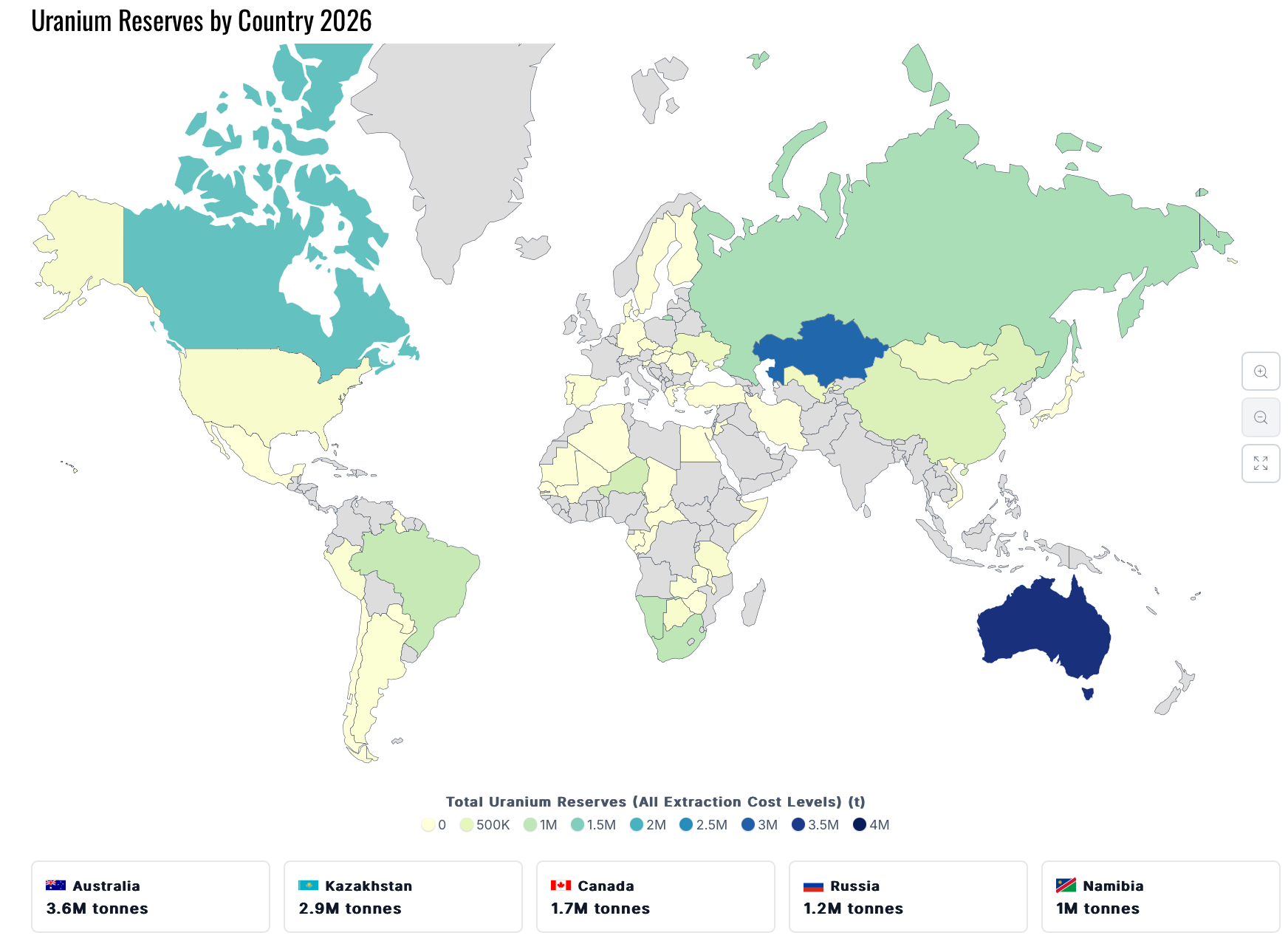

Kazakhstan is not a marginal supplier. It sits at the core of the civilian nuclear fuel cycle, producing over 40% of global uranium output and holding roughly 14% of known reserves. Control here is not symbolic. It is systemic.

What converts control into leverage is infrastructure and access. On that front, geography intrudes. Kazakhstan’s uranium base sits along the Russia–China axis: landlocked, south-weighted, and dependent on east–west corridors. Location concentrates value, but it also constrains who can move it.

Uranium power is not static. It migrates with politics, collapse, and infrastructure.

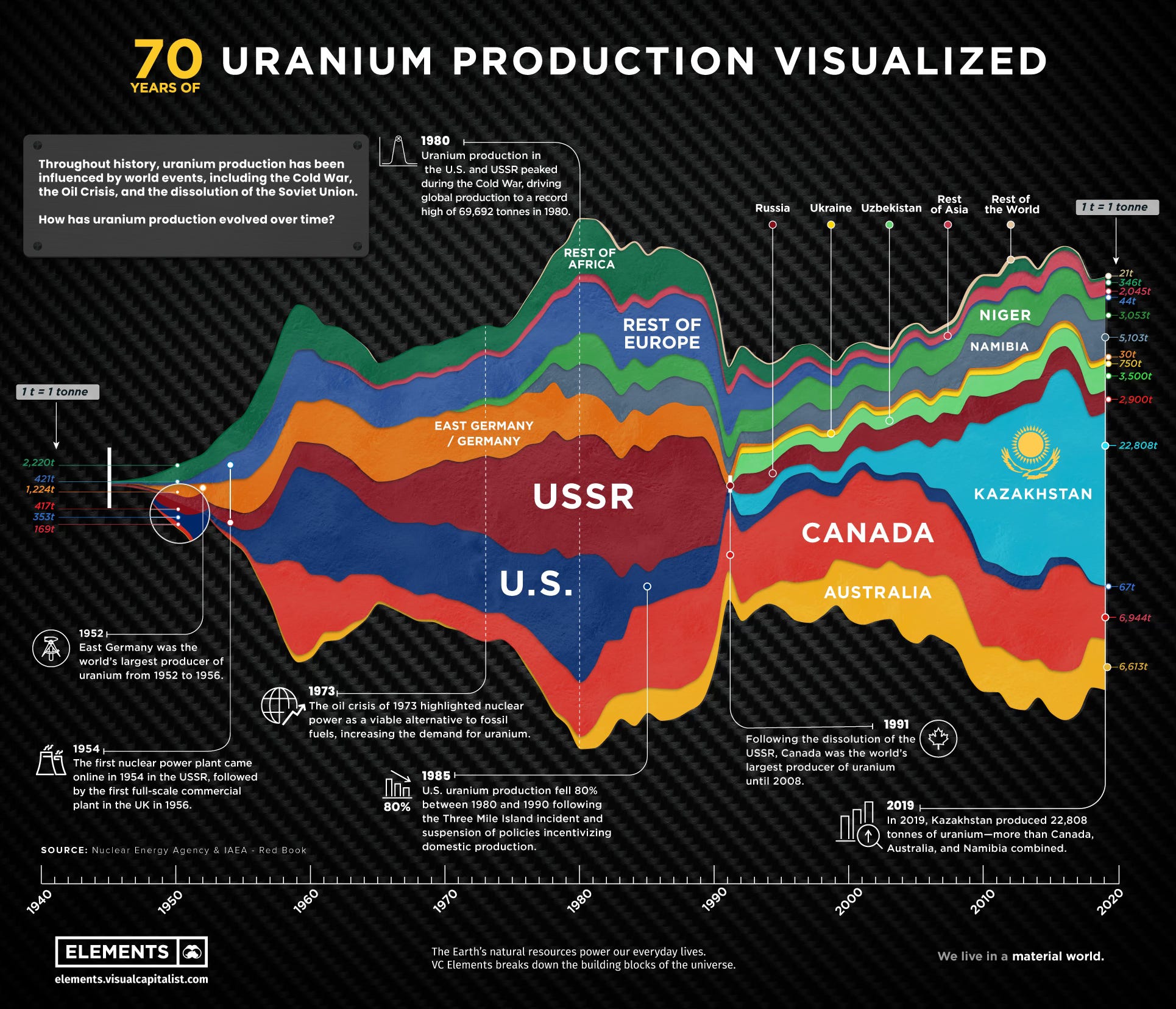

Seen in historical context, Kazakhstan’s dominance is not accidental. Global uranium production has always followed power, not price. During the Cold War, output was concentrated in the U.S. and the Soviet bloc, driven by weapons programs and early reactor build-outs.

When the USSR collapsed, that production did not disappear. It migrated. What had been dispersed across Soviet republics was gradually consolidated inside Kazakhstan, which combined favorable geology with political stability and state coordination.

The record is clear. Moscow lost territorial control over uranium production in the 1990s, but it never abandoned the nuclear system built around it. That distinction still shapes Russian strategy today.

Control over that node does not automatically translate into geopolitical leverage. But misalignment between upstream ownership and downstream infrastructure almost guarantees dependence. That gap has been visible for years, and it was filled early.

Russia and China approached it differently. Russia remained embedded through continuity, inheriting fuel-cycle integration, standards, and personnel from the Soviet system. China arrived later, but with capital discipline and a clearer sense of sequencing, tying ownership, offtake, processing, and reactor construction into a single package.

In 2025, the presidents of Russia, China, and the United States had all made a point of engaging Kazakhstan’s leadership. The convergence signaled not alignment, but competition over a shrinking set of strategic nodes.

The new legal framework reflects lessons drawn from that experience. Foreign partners are no longer invited in as passive equity holders extracting ore. Continued access now comes with conditions: technology transfer, domestic processing, long-term offtake commitments, and acceptance of Kazatomprom’s controlling role.

In theory, this resembles resource nationalism. In practice, it functions as selective alignment — and only a narrow set of actors can meet those terms without friction.

Like what you’re reading? Subscribe for free to Financial Compass to get new articles delivered straight to your inbox. 📥

Russia is one of them. In June 2025, the Kazakh Atomic Energy Agency selected Rosatom to lead construction of its first large-scale nuclear power plant near Ulken, built around VVER-1200 reactors. These projects are not turnkey purchases. They bind the host country into decades-long relationships involving fuel supply, maintenance, training, regulatory compatibility, and spare parts. Even before the first kilowatt is generated, the dependency is locked in. Sanctions have weakened Moscow’s financing capacity, but not its technical grip.

China is the other. China National Nuclear Corporation (CNNC) has been positioned to build additional reactors as Kazakhstan scales toward roughly 2.4 GW of nuclear capacity by the mid-2030s. Almasadam Satqaliev, the Kazakh agency’s chairman revealed the reason:

“China is definitely one of the countries that has all the necessary technologies and the entire industrial base, and our next main priority is cooperation with China.”

Beijing’s advantage is not just price — though Chinese bids have undercut Western competitors by billions — but scope. CNNC packages reactors with financing, fuel services, grid integration, and upstream access to uranium assets. Chinese firms already participate in key Kazakh uranium projects, ensuring that supply and consumption increasingly sit within the same strategic orbit.

This is where U.S. strategic language begins to diverge from material reality. Washington speaks of diversification, balance, and engagement. But influence in nuclear markets is not rhetorical; it is infrastructural. The United States has no enrichment footprint in Kazakhstan, no reactor projects under contract, and no binding role in fuel services. Discussions around small modular reactors, regulatory cooperation, and training programs remain preliminary, adjacent to power, not embedded in it.

Even worse, U.S. policy continues to handicap itself. The Jackson–Vanik Amendment, a Cold War artifact, still complicates full normalization of trade relations with Kazakhstan. Efforts to repeal it have stalled, signaling hesitation rather than commitment. From Astana’s perspective, this matters less as symbolism than as signal: Washington is interested, but not invested.

Washington is not unaware of this erosion. Last week, the U.S. Department of Energy committed $2.7 billion to revive domestic uranium enrichment capacity, an explicit acknowledgment that the United States allowed critical segments of the nuclear fuel cycle to atrophy:

“The U.S. Department of Energy (DOE) today announced $2.7 billion to strengthen domestic enrichment services over the next ten years. In support of President Trump’s commitment to enhance energy security and reduce reliance on foreign suppliers, the historic investment expands U.S. capacity for low-enriched uranium (LEU) and jumpstarts new supply chains and innovations for high-assay low-enriched uranium (HALEU) to create American jobs and usher in the nation’s nuclear renaissance.”

The move signals recognition, not reach. Rebuilding enrichment at home does little to alter leverage abroad, where supply, processing, and reactor systems are already locked into long-term industrial relationships. Awareness arrived late. Infrastructure did not.

The contrast with China is instructive. Where the U.S. treats billons in infrastructure requirements as politically infeasible, Beijing treats them as entry tickets. Rail links, processing facilities, industrial parks, and digital infrastructure are layered around nuclear and mineral projects, creating ecosystems rather than standalone assets. Control does not require ownership of everything, only of the choke points that matter in a crisis.

Kazakhstan’s tightening grip over uranium should therefore not be read as a pivot toward Western alignment. It is an attempt to rebalance leverage between foreign partners, but the partners best positioned to operate under the new rules are the same ones already dominant. Russia brings legacy integration and technical depth. China brings capital, speed, and a willingness to accept long time horizons. The United States brings interest, but little that alters the underlying structure.

The real risk for Washington is not exclusion, but irrelevance by default. Kazakhstan will continue to speak the language of multi-vector diplomacy, and there is no reason to doubt its sincerity. But vectors are not chosen by speeches. They are determined by infrastructure, contracts, and who shows up with capital when decisions are irreversible.

By consolidating state control now, Astana is ensuring it captures more value from its uranium endowment. By choosing Russian and Chinese partners to operationalize that control, it is also narrowing its future room for maneuver. And by failing to anchor itself in those decisions, the United States is learning, again, that strategic interests declared too late tend to remain theoretical.

The uranium is Kazakh. The leverage increasingly is not.

This article comes at the perfect time. Given this systemic state control over such a critical resource, how do you foresee the long-term geopolitcal impacts on global energy security? Your analysis is incredibly sharp and insightful, connecting the dots on power shifts so clearly.

This is a thoughtful and sobering read. What really stands out is how clearly it shows that power in commodities doesn’t come from ownership alone, but from who controls the pipes, the timelines, and the commitments once choices become irreversible.

It’s a strong reminder that “engagement” without infrastructure is mostly symbolism, and that in strategic markets, leverage quietly shifts long before it’s visible in prices or headlines. Excellent take. Worth thinking about!