Industrial Alchemy

Saudi Arabia is repositioning itself around the critical mineral chokepoint

In the late nineteenth century, aluminum was a luxury more precious than silver. Napoleon III famously reserved aluminum cutlery for his most honoured guests, while lesser dignitaries made do with gold. Though aluminum is the most abundant metal in the Earth’s crust, that geological reality mattered little because no one had discovered a way to separate it economically from bauxite ore.

This changed with the invention of the Hall–Héroult process. Almost overnight, a curiosity of the elite became the backbone of industrial civilisation, paving the way for aircraft, transmission lines, skyscrapers, and modern warfare.

The breakthrough was not a discovery of new land, but a triumph of chemical processing.

Although rare earth elements are not nearly as abundant as aluminum, they occupy a strikingly similar strategic position today. Despite their name, the world is not (yet) facing a shortage of physical deposits; rather, it faces a crippling deficit in refining capacity. The strategic bottleneck no longer lies only in discovering minerals, but in separating, processing, and transforming them into usable industrial inputs.

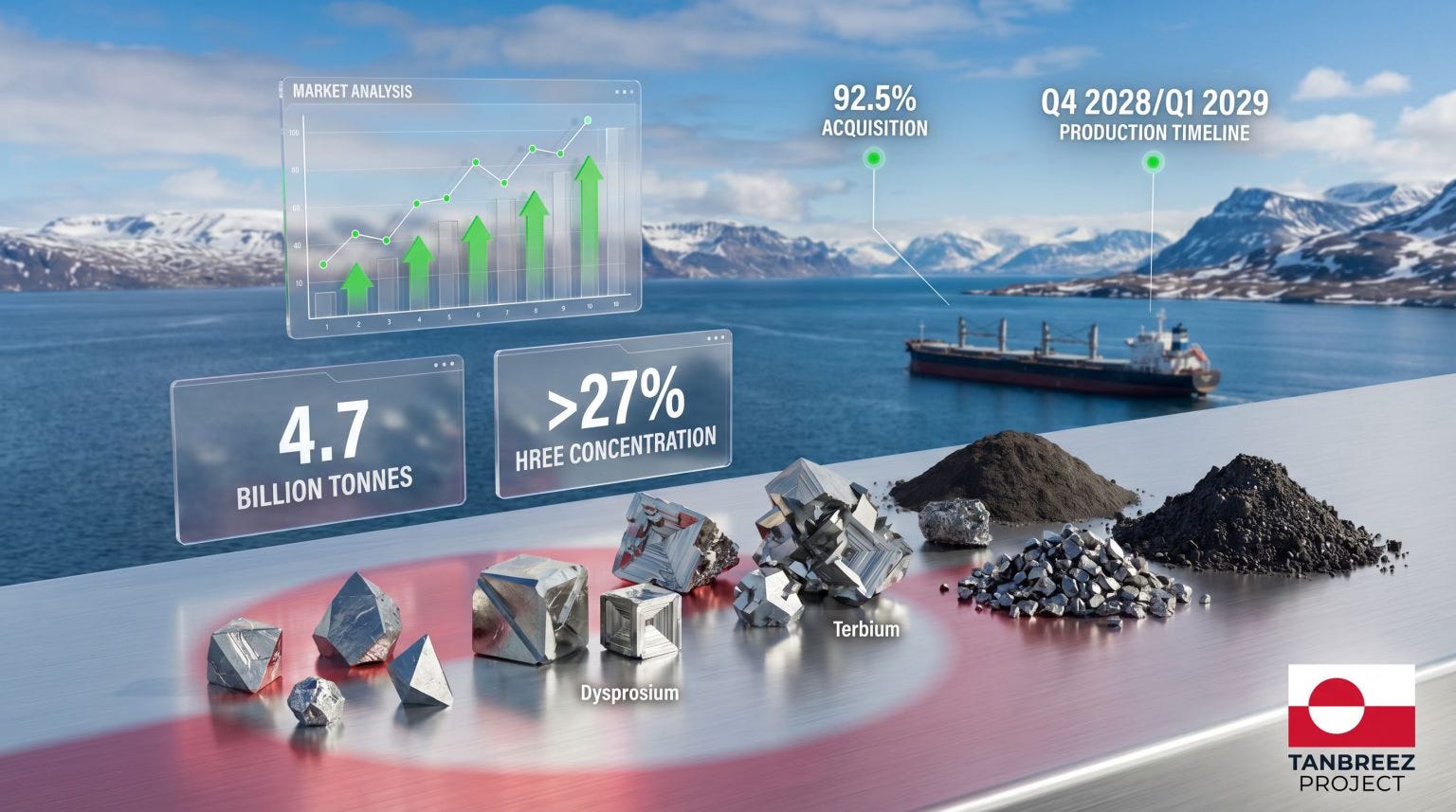

This brings us to the Tanbreez project in southern Greenland, recently acquired by U.S.-based Critical Metals Corp. — one of the West’s most ambitious attempts to secure a non-Chinese rare earth supply chain. The headlines have been dominated by the sheer scale of this discovery, and the numbers justify the noise. The deposit is estimated to contain 4.7 billion tonnes of multi-element ore, including 28.2 million tonnes of rare earth oxides.

It is being hailed as one of the largest deposits on the planet, with a specific emphasis on heavy rare earth elements (HREE), which make up an unusually high 27% of the total rare earth mix. We are talking about the most critical materials for our technological future: dysprosium and terbium, which allow magnets to function at high temperatures, and yttrium, essential for lasers and superconductors.

However, as impressive as these deposits are, they are effectively useless without refining. A mountain of ore in the Arctic is just heavy rock until someone performs the chemical alchemy required to extract the value. What is striking—and far less discussed—is who is likely to do that work: Saudi Arabia.

Critical Minerals Corp signed a preliminary agreement with Saudi firm Al Qahtani & Brothers to refine up to 25% of output from Greenland’s Tanbreez rare earth project inside the Kingdom. Said Bakr, a research associate at the Arab Gulf States Institute, described the move as a major strategic opportunity for Saudi Arabia:

“If that agreement ultimately materialises and Tanbreez material is processed in Saudi Arabia, it would give the kingdom a role in one of the most strategically important stages of the critical minerals supply chain.”

Readers of this publication already know that Saudi Arabia does not want to remain trapped inside the old rentier-state model — a system where the state provides prosperity through oil wealth in exchange for political passivity. Saudi Arabia understands that oil alone no longer guarantees its future. Hydrocarbon wealth created modern Saudi Arabia, but the Kingdom increasingly recognises that the next industrial cycle will revolve around processing, manufacturing, AI infrastructure, electrification, and strategic materials — a realisation now embedded into Vision 2030.

Relying on oil as a single, volatile revenue stream is a dangerous game in a world where the geopolitical weather turns on a dime. With disruptions in the Strait of Hormuz threatening market stability until 2027 and the production cut of up to 2 million barrels per day, being "just" an oil kingdom is a precarious position.

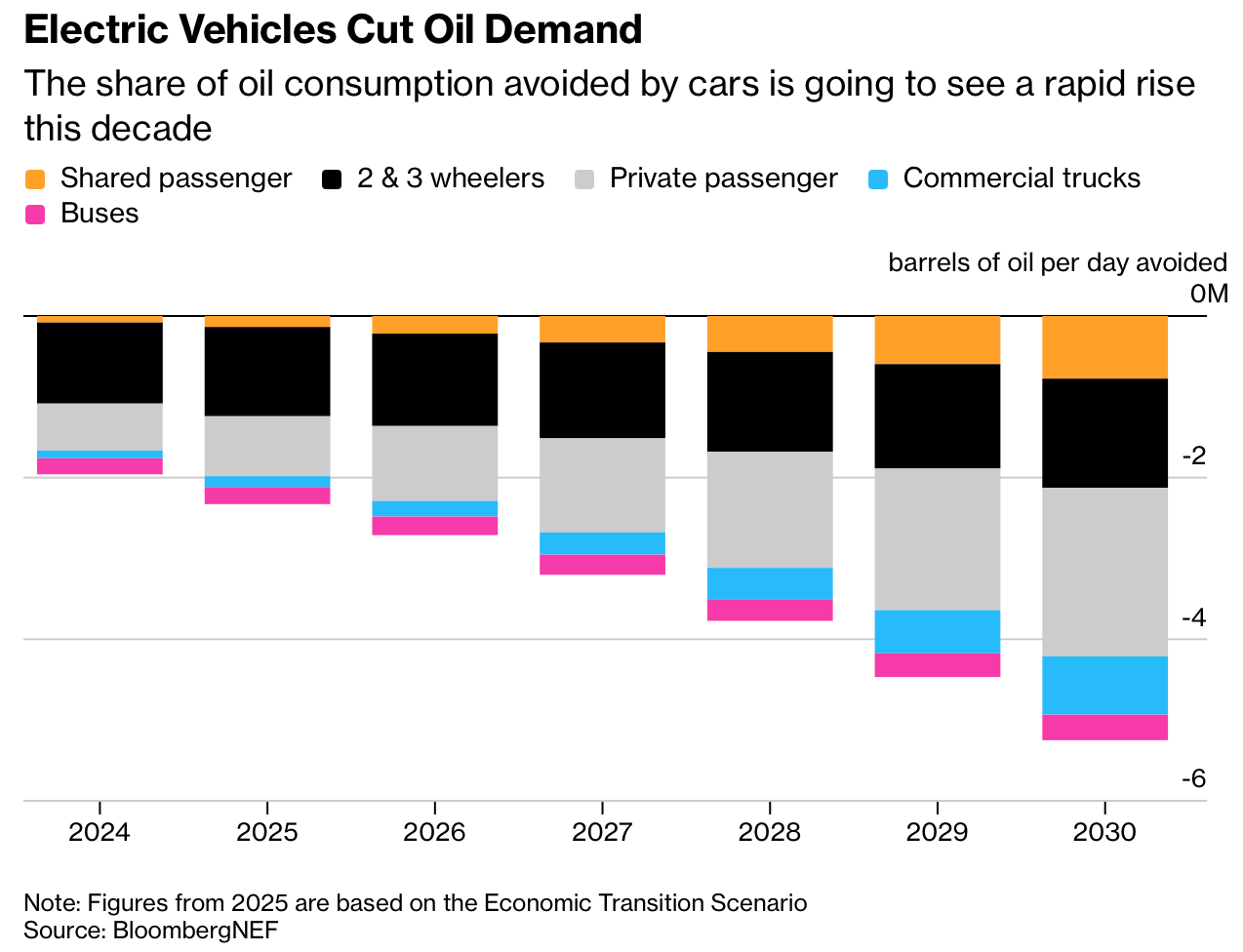

The underlying economic transformation is relentless. Despite the shifting political winds in the West and the rollback of various sustainability goals, the decline in oil demand is already baked into the future. The electrification of transport alone is projected to erase millions of barrels of daily oil demand by 2030.

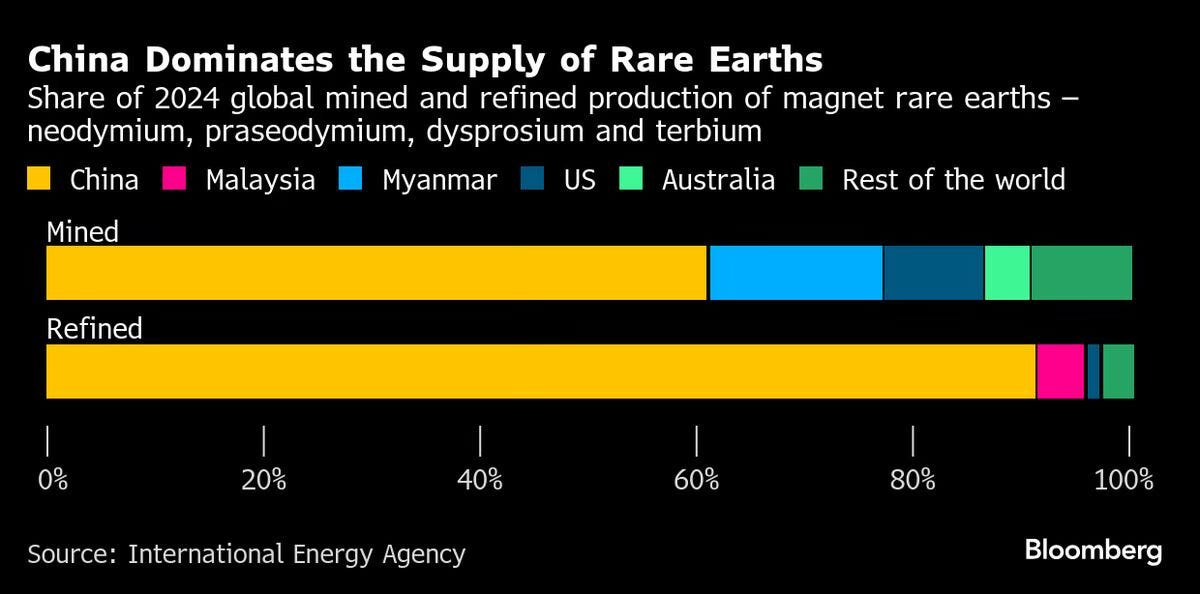

Saudi Arabia sees the writing on the wall. With China currently controlling 90% of the rare earth refining market, the Kingdom is positioning itself as an emerging alternative within the West’s search for new processing capacity. They are diversifying from a resource the world is gradually trying to reduce dependence on toward industrial capabilities the future economy cannot function without. It is the ultimate strategic hedge: owning the crucible that will forge the next industrial age.

This strategic pivot was formalised through a landmark cooperation agreement between the U.S. and Saudi Arabia, marking a new era of industrial diplomacy where the Kingdom serves as a critical link in the Western supply chain. For the United States, this partnership offers a detour around domestic delays and high labor costs; for Saudi Arabia, it provides the technical expertise to move up the value chain. This marriage of American intellectual property and Saudi infrastructure capital is specifically designed to decouple global supply chains from China.

The most concrete development of this shift so far was the 2025 joint venture between MP Materials and Saudi state-backed mining company Ma’aden. By establishing a rare earth refinery in Saudi Arabia, MP Materials—operator of the Mountain Pass mine—gains access to low-cost energy and massive capital reserves. Electricity costs in the Kingdom average roughly $0.025–0.035 per kilowatt-hour, well below most industrial economies, while rare earth separation itself can require 500–1,000 kilowatt-hours per tonne of processed material.

The existential importance of this infrastructure is underscored by the U.S. government’s decision to take a direct 15% stake in MP Materials earlier this year, effectively classifying these refining partnerships as matters of national security. By anchoring Greenland’s Tanbreez output and MP Materials’ refining capacity in the Middle East, Saudi Arabia is creating a trans-continental mineral corridor.

The Kingdom isn’t just looking to refine raw materials; it wants to control larger parts of the industrial value chain. This ambition sits at the heart of Vision 2030, which aims to transform Saudi Arabia from a pure oil exporter into a strategic logistics, manufacturing, and energy hub. That strategy is increasingly visible in projects like the $500 billion NEOM development, envisioned as a post-oil industrial corridor linked to advanced manufacturing, renewable energy, and large-scale battery storage infrastructure.

Projects like The Line — the proposed 170-kilometer, car-free, zero-carbon smart city — and Oxagon, a reimagined industrial city on the Red Sea, are being designed to integrate directly into this broader economic transition. Rather than functioning solely as futuristic showcase projects, they are intended to anchor new supply chains across refining, maritime trade, clean energy, and advanced materials. Saudi policymakers increasingly understand that future wealth may depend less on extracting resources than on controlling the systems that process, transport, and industrialise them.

Yet Saudi Arabia’s transformation may also reflect geological pressure, not just ambition.

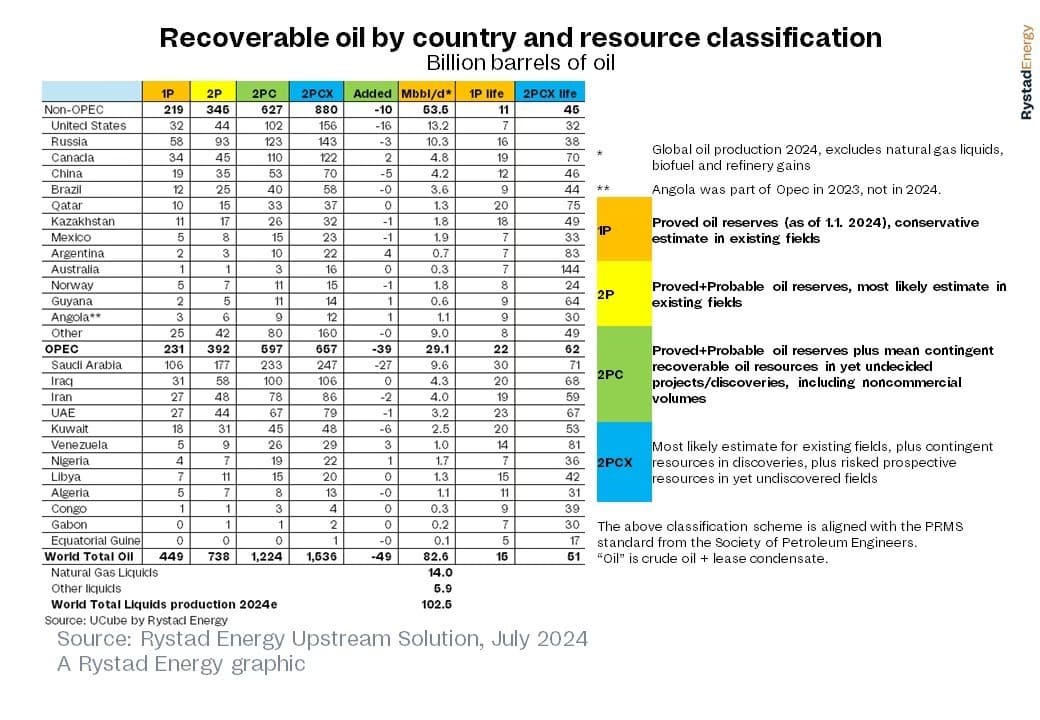

Analysis citing Rystad Energy argued that OPEC’s recoverable reserves may be closer to 657 billion barrels rather than the roughly 1.2 trillion barrels officially reported. Saudi Arabia sits at the center of that debate, having seen some of the largest downward reserve revisions. The Kingdom’s official reserves have remained near 260 billion barrels since the late 1980s, despite producing more than 130 billion barrels of oil over that same period — a consistency that has increasingly raised doubts among many respectable independent analysts.

If even partially correct, Saudi Arabia’s push into rare earth mining, refining, and industrial diversification begins to look less like optional modernisation and more like strategic preparation for a future in which oil no longer guarantees the same economic and geopolitical leverage it once did. In many ways, that erosion had already begun with the U.S. shale revolution, which sharply reduced American dependence on Saudi crude and weakened one of the foundational pillars of the traditional U.S.–Saudi relationship.

Saudi Arabia’s push into rare earths, refining, and industrial infrastructure should not be mistaken for a leisurely modernization project. It increasingly resembles a strategic repositioning effort — one quietly supported by Washington as the United States searches for alternatives to Chinese mineral dominance without fully rebuilding the industrial chain at home. The Saudis themselves are making little secret of these ambitions, increasingly presenting the Kingdom’s estimated $2.5 trillion in untapped mineral reserves as the foundation for its next economic era.

The Kingdom is attempting to diversify from the hydrocarbon system that defined the twentieth century toward the critical mineral infrastructure expected to underpin the twenty-first. Saudi policymakers increasingly understand that future geopolitical leverage may belong not only to those who can extract resources, but even more to those who control the refining capacity, processing networks, and industrial chokepoints that the West still lacks.

Yet until these sectors generate meaningful economic gravity of their own, Saudi Arabia remains deeply dependent on the very hydrocarbon system it is trying to move beyond.

Subscribe to receive my posts directly in your inbox and support my work!

Share this with anyone if you think their attention span can survive more than two paragraphs — and if not, send it anyway. 📨

This sounds like a smart move for the Saudis. I’m going to assume that the process of refining these elements requires much heat so therefore it would be less efficient to do in Canada. Otherwise, that would be the logical location to set up a new refining operation.

Forgot to mention - very interesting article. Thank you