Power Divide

The AI race may have been decided decades ago

Following the Xi–Trump summit, most of the discussion around the US-China AI race still revolves around chips, models, and technological leadership. Washington continues to frame artificial intelligence as a technological arms race where a few months of algorithmic superiority supposedly determine geopolitical dominance. But the center of gravity is quietly shifting underneath the entire discussion. Artificial intelligence is becoming an energy story.

The United States still leads at the frontier of AI development. According to data highlighted by Time Magazine, Chinese frontier AI models have trailed American systems by roughly seven months since 2023. But technological advantages compress quickly once ecosystems mature, open-source architectures spread, and engineering talent circulates globally.

Infrastructure does not move that way. A company could close a software gap within months, but a nation cannot build hydroelectric dams, ultra-high-voltage transmission corridors, transformer manufacturing ecosystems, and continental power grids within the same time. Technology is easier to catch up in than energy infrastructure, and that distinction increasingly favors China.

The uncomfortable reality emerging inside the AI race is that the limiting factor is no longer purely computational intelligence. It is electricity generation. Every large language model (LLM) is fundamentally a machine that converts electricity into computation. As AI becomes embedded deeper into the day-to-day functioning of modern economies, the demand for electricity increasingly becomes structural rather than cyclical.

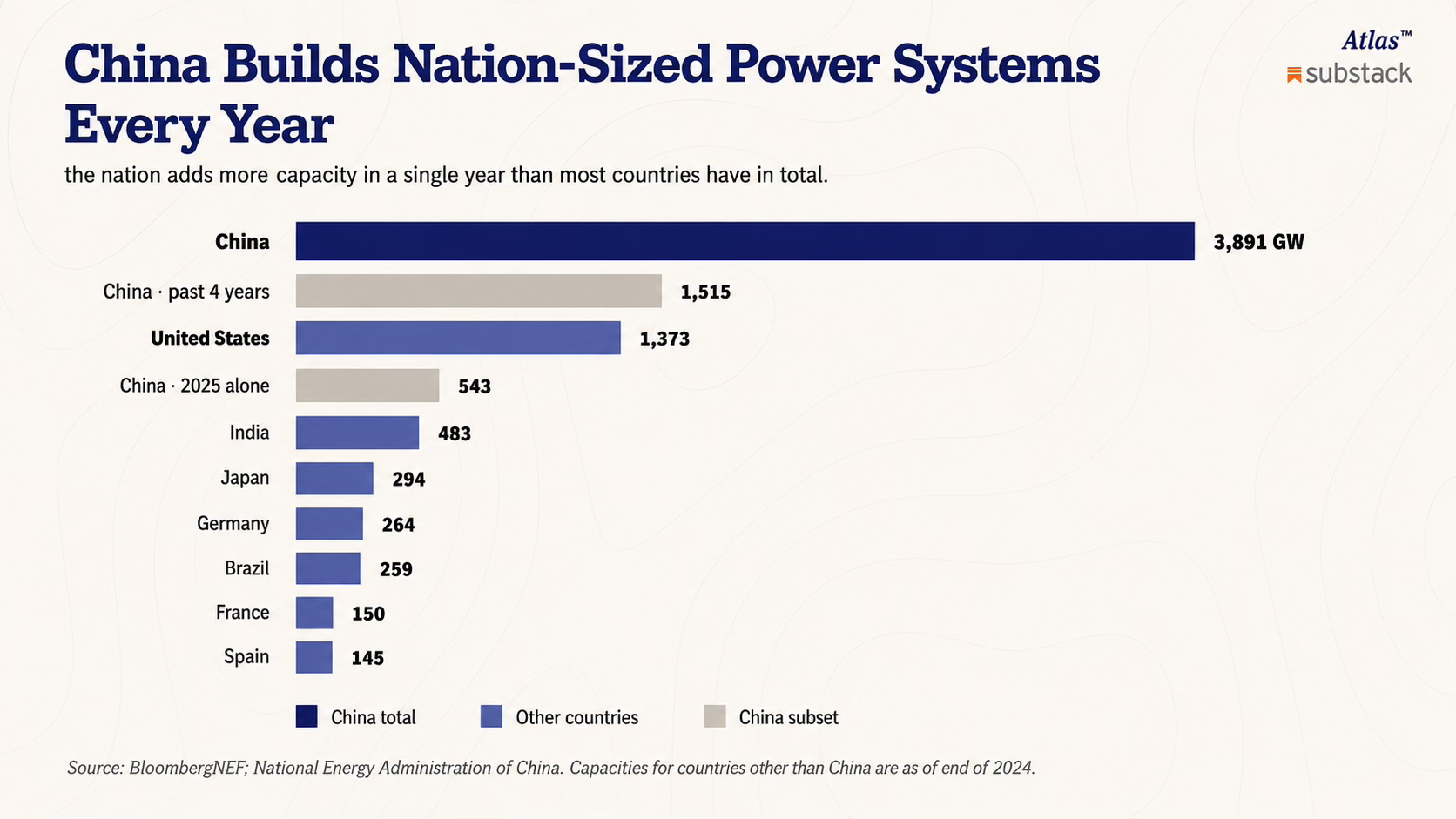

China appears to have understood this before almost anyone else. Since 2021, China has added more power generation capacity than the United States built across its entire history. In 2025 alone, China added 543 gigawatts of electricity capacity. Total installed Chinese capacity now stands near 3,900 gigawatts versus roughly 1,500 gigawatts for the United States.

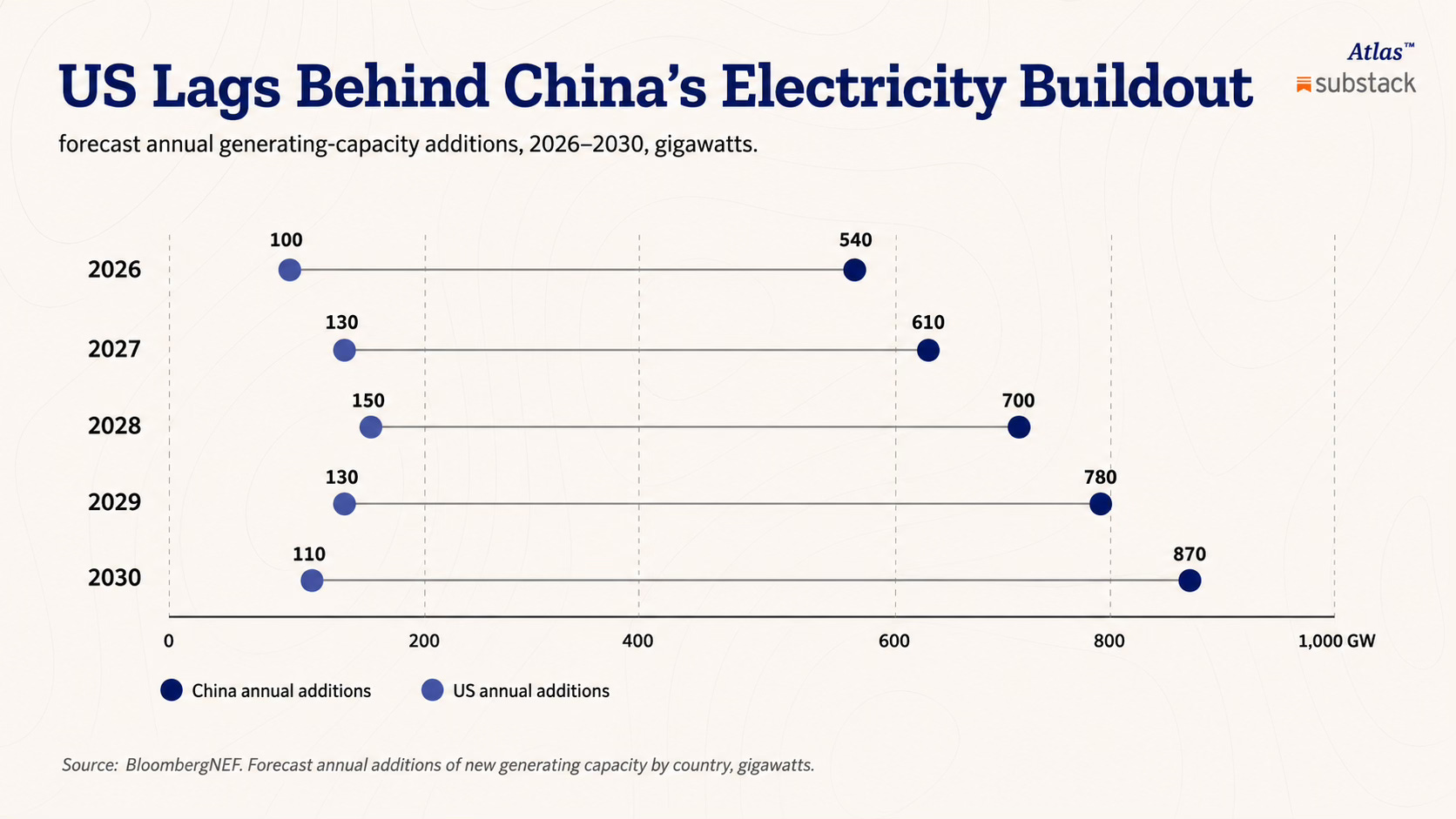

Over the next five years, China is projected to add another 3.4 terawatts of generation capacity, nearly six times more than the US. The trajectory itself matters even more than the aggregate numbers. China is projected to add roughly 540 gigawatts of new capacity in 2026, rising toward 870 gigawatts annually by 2030. The United States, by comparison, is expected to fluctuate between roughly 100 and 150 gigawatts annually over the same period. China is not merely building more power infrastructure than the United States. It is building on an entirely different scale of industrial mobilization.

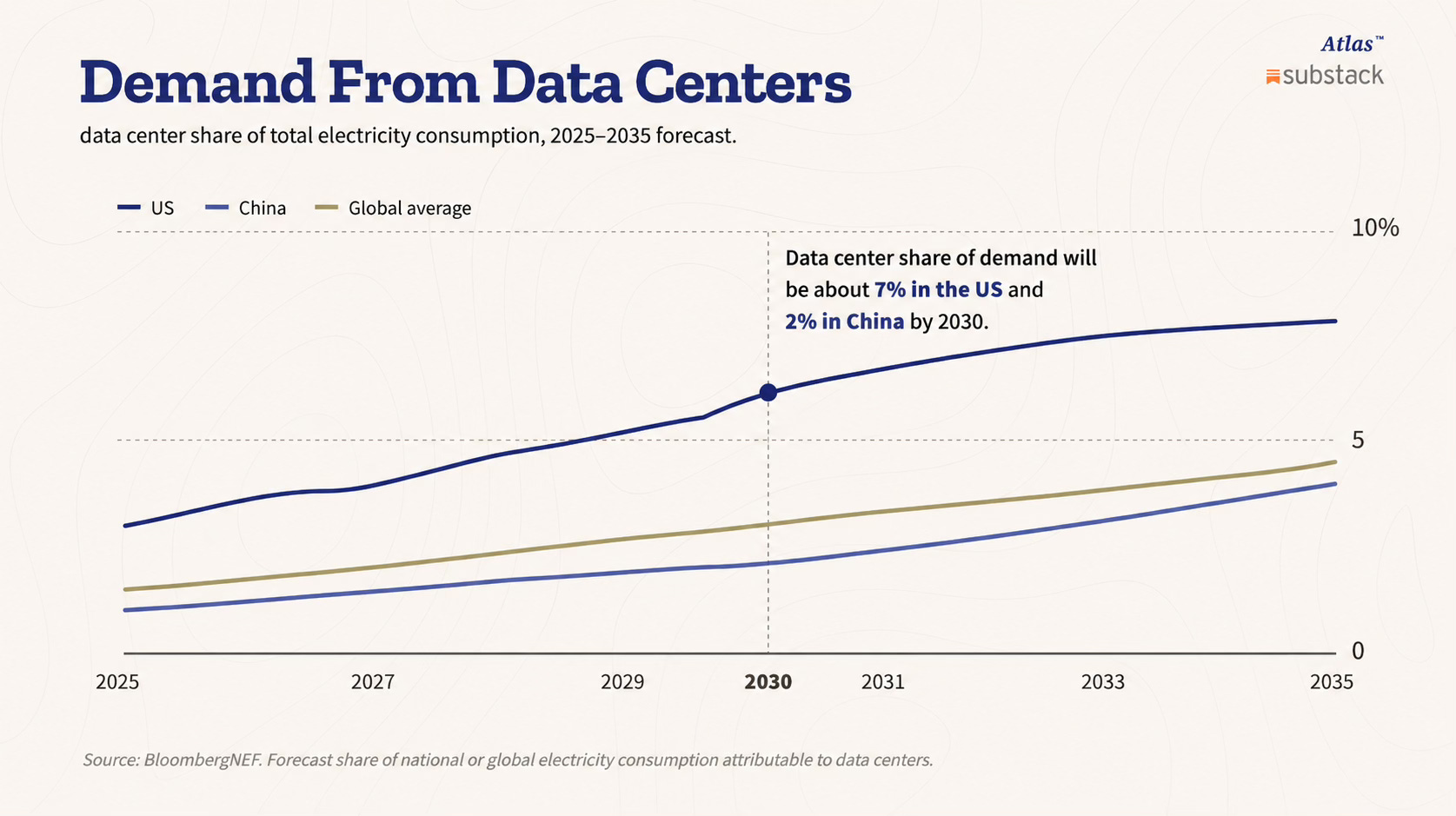

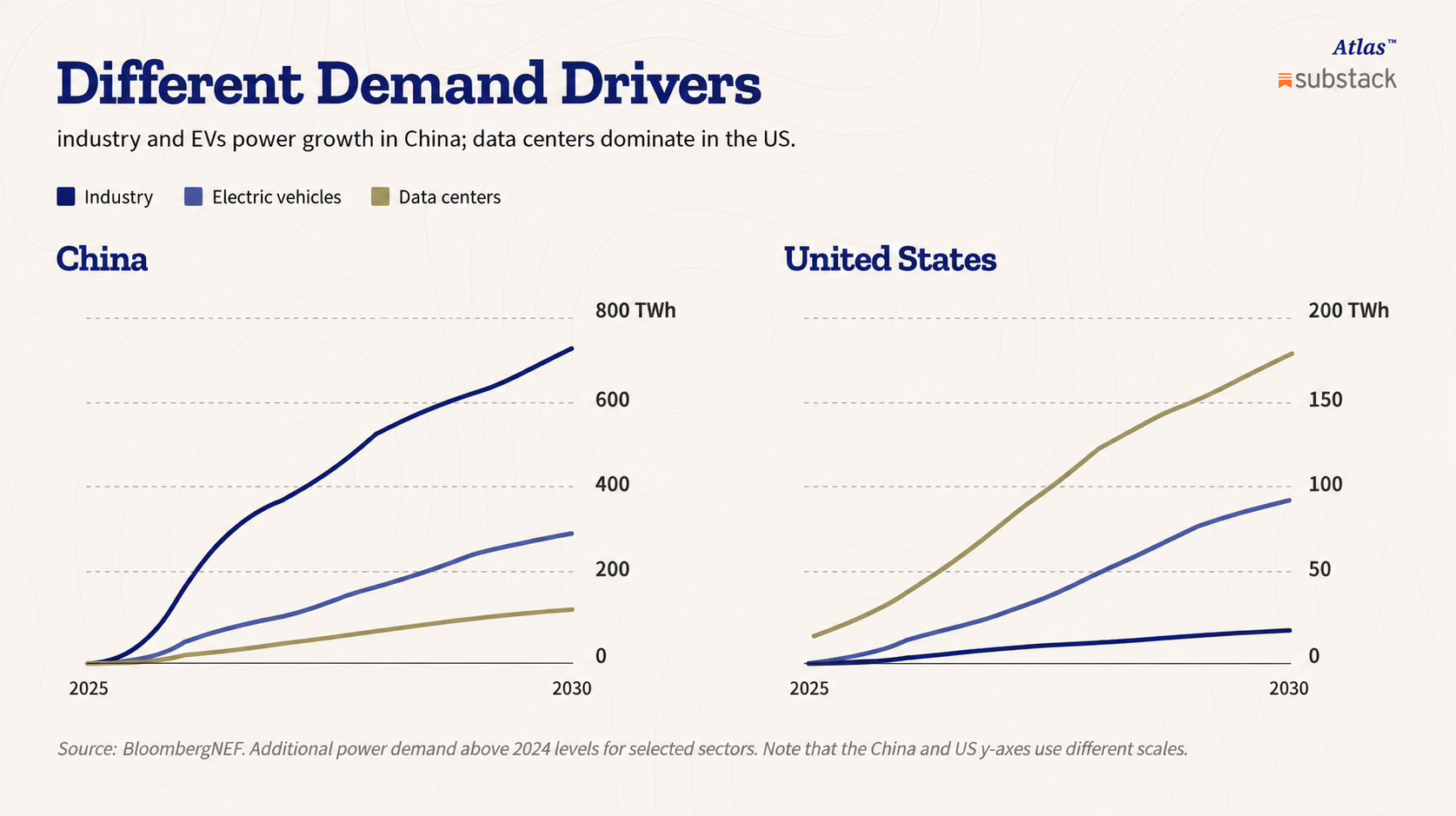

Those numbers stop sounding normal after a while because China is no longer operating at the scale of ordinary infrastructure expansion. It is effectively constructing nation-sized power systems every few years. This matters because AI infrastructure is unbelievably power hungry. By 2030, data centers are projected to account for roughly 7% of total US electricity demand, versus only around 2% in China. That divergence reveals something deeper than just different AI adoption curves.

In the United States, data centers increasingly dominate incremental electricity demand because the broader industrial base has remained relatively stagnant for decades. In China, AI demand is being absorbed into a much larger expansion cycle driven simultaneously by industrial electrification, electric vehicles, heavy manufacturing, and nationwide infrastructure buildouts.

The contrast is becoming structurally important. Chinese industrial demand growth alone is projected to add nearly 700 terawatt-hours of electricity consumption by 2030. Electric vehicles add another roughly 300 terawatt-hours. Data centers remain comparatively small within the broader Chinese system. In the United States, meanwhile, data centers increasingly dominate new demand growth almost by themselves.

The old assumption was that the AI race would be won by whoever designed the best chips. Increasingly, it may instead be won by whoever can sustain the largest concentrations of electricity demand without destabilizing the grid. Elon Musk recently acknowledged during a conversation with Larry Fink at the World Economic Forum that the primary constraint on AI deployment is no longer chips, but electrical power itself:

“Very soon, maybe even later this year we’ll be producing more chips than we can turn on — except for China. China’s growth in electricity is tremendous.”

Jensen Huang made essentially the same point, describing energy as the foundational layer beneath chips, models, and applications.

That is where the conversation becomes strategically uncomfortable for the United States. China spent decades building energy systems with thirty-year timelines. The United States spent decades optimising for short-term returns, political cycles, and shareholder efficiency. One side continued constructing industrial infrastructure at continental scale while the other increasingly treated infrastructure as an environmental dispute or partisan culture war.

Although it’s true that China’s primary source of power generation remains coal, the country has invested heavily in renewable energy to diversify its energy mix. Renewables and nuclear power are expanding rapidly, reflecting a willingness to pursue large-scale projects with decade-long timelines in pursuit of long-term energy security.

The Three Gorges Dam —the largest hydroelectricity dam in the world by far— illustrates the difference perfectly. Construction stretched across more than a decade, beginning in 1994 and reaching completion in 2012. The project became one of the largest infrastructure undertakings in modern history. Today, the dam contributes roughly 1.5% to 3% of China’s total electricity generation depending on annual water conditions.

At first glance, that may sound surprisingly small relative to the enormity of the project. But that interpretation misses the point entirely. The importance of Three Gorges is not simply the percentage of national generation. The importance is that a single infrastructure asset can contribute electricity at civilizational scale for generations. The project reflects a political system willing to think in half-century timelines rather than the short-term electoral cycles that increasingly shape infrastructure planning in much of the West.

That mentality compounds over time. China did not just build hydroelectric dams. It simultaneously built solar manufacturing dominance, nuclear capacity, coal backup systems, ultra-high-voltage transmission corridors, battery supply chains, and transformer manufacturing ecosystems.

On the Tibetan Plateau, China is even constructing solar parks so large they exceed the size of Manhattan, turning entire regions into utility-scale power systems designed for decades of future electrification. The result is not merely more electricity. The result is optionality.

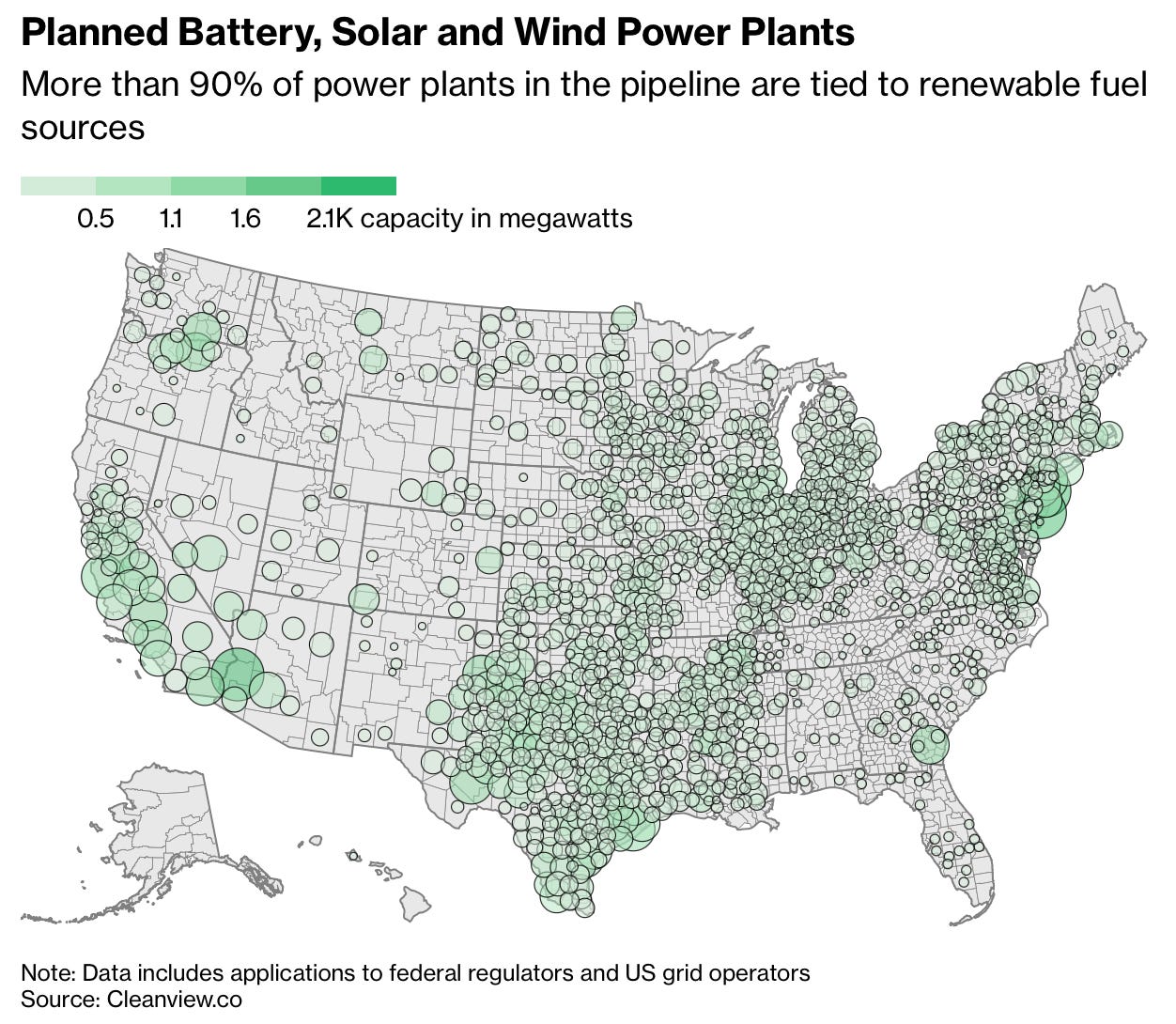

The United States increasingly lacks that flexibility. Washington wants to dominate artificial intelligence while simultaneously attacking the fastest-growing segments of its own power infrastructure. President Trump continues positioning himself aggressively against wind and solar energy despite the simple logistical reality that renewables now dominate America’s future power additions.

More than 90% of power plants currently in the US development pipeline are tied to renewable energy sources, primarily solar, wind, and battery storage systems. Roughly 34% of planned capacity comes from solar, another 34% from battery storage, and 11% from wind. Natural gas accounts for only around 13%.

Renewables are simply the fastest systems to deploy at scale. Large solar, battery, and wind projects can sometimes be completed within 18 months to five years. Gas plants increasingly face turbine shortages and supply chain delays. Nuclear projects remain extraordinarily slow and expensive. Coal has become structurally uncompetitive. New coal generation now costs roughly $71 per megawatt-hour compared with around $38 for solar or wind. The irony is difficult to ignore. America’s AI ambitions increasingly depend on infrastructure categories its own political system keeps attempting to slow down.

That contradiction now runs through the entire US grid. Data centers in parts of Virginia reportedly face waits of up to seven years for grid connections. Offshore wind projects repeatedly encounter federal resistance despite judges continuously overturning stop-work orders. Orsted, the Danish energy giant that is building Sunrise Wind near New York was losing $2.5 million per day while frozen in legal limbo.

Meanwhile electricity demand is beginning to surge after nearly two decades of relative stagnation. The United States now faces a structural mismatch between AI deployment speed and infrastructure deployment speed. Hyperscalers can construct enormous data centers rapidly because capital moves quickly. Electrical generation and transmission systems do not. That mismatch increasingly benefits China because China spent years building ahead of demand.

This is also why the semiconductor story itself is beginning to change faster than many in Washington expected. The assumption behind export controls was that restricting Nvidia’s most advanced GPU’s would preserve a durable American lead. But recent developments increasingly suggest China may already be much closer than the market assumes.

After the Trump administration approved exports of Nvidia’s H200 GPU’s to China earlier this week, Beijing reportedly chose not to move forward with purchases because it wants to accelerate domestic alternatives instead. Trump himself acknowledged that China “chose not to” buy the chips because “they want to develop their own.”

That is an important strategic signal. If China truly believed it remained hopelessly dependent on American hardware for the foreseeable future, refusing access to Nvidia’s H200 chips would make little sense. The fact that Beijing appears increasingly comfortable prioritising domestic ecosystems suggests Chinese capabilities may already be advancing faster than many Western narratives imply.

Technology gaps can compress surprisingly quickly once industrial ecosystems mature. Infrastructure gaps do not. A Chinese AI model that trails an American frontier model by seven months today may narrow that difference within months or years. But if China simultaneously possesses vastly larger electricity reserves, denser industrial ecosystems, faster transmission deployment, larger transformer production, and integrated manufacturing capacity, then software parity changes the strategic equation entirely.

At that point, deployment scale becomes decisive. Who can continuously train larger models without destabilizing national grids? Who can absorb exponential electricity growth without multi-year interconnection queues? Who can industrialize AI across robotics, manufacturing, logistics, defense systems, and surveillance infrastructure simultaneously? Those are infrastructure questions.

The uncomfortable implication is that the foundations of the AI race may have been laid long before the AI boom itself began. While Washington focused on preserving technological leadership through chips and software, China spent decades expanding the physical systems underneath industrial power itself.

Artificial intelligence is now exposing the difference between inventing technology and scaling it across an entire civilization. In the end, the decisive advantage may not belong to whoever builds the smartest model first, but to whoever can sustain the energy, infrastructure, and industrial capacity required to deploy intelligence at national scale.

Subscribe to receive my posts directly in your inbox and support my work!

Share this with anyone if you think their attention span can survive more than two paragraphs — and if not, send it anyway. 📨

The Three Gorges dam appears to have been vulnerable on seperate occassions. Due to excessive rainfall. Dependancy is a risk to the Chinese society. Solar and wind, gas and coal turbines and nuclear power may mitigate this risk.

Appreciate you underscoring the impact of LT planning!,