Southbound

Europe’s break from Russian gas is turning Greece into the backbone of a new dependency on the United States

The shifting geography of European energy security has a knack for transforming peripheral states into self-proclaimed geopolitical linchpins. The latest nation to audition for this role is Greece, a country currently repositioning itself as the southern gateway for Europe’s natural gas market.

Against a backdrop of global energy shocks, including volatile conflicts in Ukraine and Iran, and a transactional Trump administration pushing for American energy dominance, Athens has found a lucrative, if precarious, niche. By expanding its LNG capacity and championing infrastructural networks, Greece aims to channel transatlantic supplies into Central and Eastern Europe, ostensibly replacing the continent's historic reliance on cheap Russian gas.

The narrative coming out of Athens is one of triumph and regional leadership. Yet, when one scratches beneath the surface of this ambitious energy hub strategy, the structural, financial, and geopolitical contradictions suggest that Greece may be constructing a house of cards—one where Europe has not escaped dependency, but merely traded one master for another.

To understand the scale of Greece’s ambition, we must look at the dramatic reorganisation of Europe’s broader energy architecture. Before Moscow’s full-scale invasion of Ukraine in 2022, the European Union relied on Russia for roughly 50% of its natural gas, delivered securely and affordably through an intricate web of legacy pipelines. The subsequent geopolitical rupture forced Brussels into a frantic decoupling exercise, cutting Russian gas imports by about two-thirds within 3 years, so that by 2025, Russia accounted for a mere 12% of total EU gas imports.

While Eurocrats routinely laud this shift as a victory for Western alignment, it exposed a glaring vulnerability in Europe’s domestic strategy. Despite decades of lofty rhetoric regarding an accelerated green transition, the reality on the ground has been stubbornly resistant to change. The shift away from fossil fuels has moved neither as quickly nor as smoothly as Brussels had hoped, leaving around 30% of European households still dependent on gas to heat their homes.

With fossil fuels remaining a stubborn fixture of the continent’s energy mix, and the European Union firmly committed to a total phase-out of Russian gas by the end of 2027, a massive supply deficit emerged. Norway stepped up to become the bloc’s largest gas supplier, providing nearly one-third of all imports by 2025. The second slot, however, was quickly claimed by the United States, which now supplies more than a quarter of the European Union's gas via seaborne LNG. This rapid pivot turned LNG into a structural pillar of European energy security for 2 main reasons.

First, it offered the illusion of diversification, allowing member states to purchase tankers from various global partners rather than being chained to a one state-owned pipeline. Second, while traditional pipelines require years of construction and excruciatingly complex geopolitical alignments, LNG infrastructure, especially floating storage and regasification units, can be deployed with relative speed. Seizing on this logistical loophole, Brussels encouraged member states to aggressively expand import capacities. European capacity increased by 70 billion cubic meters between 2023 and 2024 alone, with an additional 60 billion cubic meters projected to come online by 2030.

This infrastructure boom triggered an unprecedented financial windfall for American energy companies. Between 2004 and 2024, the value of United States oil and liquefied natural gas exports to Europe skyrocketed from a modest $1.6 billion to a staggering $90.8 billion. Over that same period, Europe’s share of total American energy exports doubled, rising from 15.2% to more than 30.5%.

Today, the United States, which only began exporting LNG at scale in 2016, supplies roughly 60% of Europe’s total LNG imports. For the most part, this supply has flowed into 13 European Union member states, concentrated heavily in Western European nations like France, Spain, and the Netherlands, which possess dense interconnector networks and established coastal entry points.

The expansion of this transatlantic energy dependency is poised to accelerate under the current Trump administration, though on terms that feel more extractionary than cooperative. President Donald Trump has consistently criticized Europe’s heavy investments in renewable energy, arguing that the continent’s green mandates have harmed both the American and European economies. During his speech at Davos, Trump offered few conciliatory words toward Europe’s green transition:

“There are windmills all over Europe. There are windmills all over the place and they are losers. One thing I’ve noticed is that the more windmills a country has, the more money that country loses and the worse that country is doing.”

In his push for absolute American energy dominance, Washington has successfully levered its supply advantages into binding trade agreements. As part of a major trade deal announced between the European Union and the United States in July 2025, Brussels pledged to purchase $250 billion worth of American oil, gas, and nuclear energy over the subsequent 3 years. In exchange, Washington offered a conditional reduction on tariffs for European goods, lowering them from 30% to 15%.

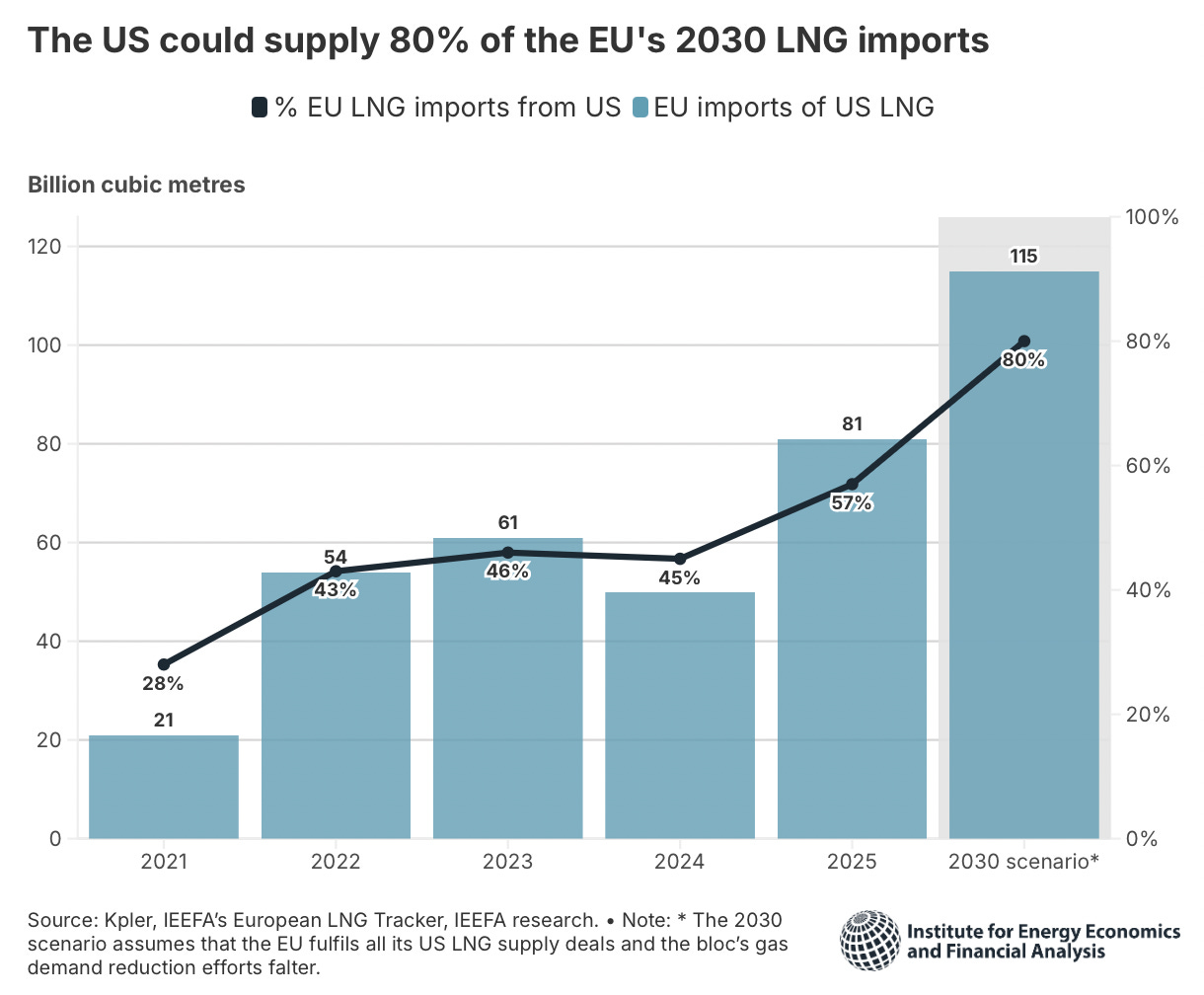

The economic arithmetic behind this arrangement, however, invites deep skepticism. Industry analysts, including those at the Institute for Energy Economics (IEE) and Kpler, suggest that the United States could supply as much as 80% of Europe’s liquefied natural gas by 2030.

The math behind this $250 billion transatlantic energy pledge exposes it as a political fantasy. For Europe to absorb that volume of American energy within just three years, it would require a massive increase in import levels. Arturo Regalado, senior LNG analyst at Kpler, argues that Brussels’ ambitions far exceed current market realities:

“U.S. oil flows would need to fully redirect towards the EU to reach the target, or the value of LNG imports from the US would need to increase sixfold.”

Realistically, such an abrupt scaling up appears operationally and logistically impossible. Nevertheless, European leaders, trapped in a geopolitical corner, used the post-deal industry summit in Washington to reaffirm their unyielding commitment to buying American gas, regardless of the structural strain.

It is precisely within this gap between political ambition and logistical reality that Greece is attempting to carve out its future. Athens is openly lobbying to become the primary southern European gateway for American LNG, aiming to transform itself from a historic energy consumer into a critical regional hub. Historically, Greece was no different from its neighbors, relying heavily on Russian oil and gas while exploiting its own polluting domestic coal mines. But as the country began phasing out coal, it sought alternative bridges, turning to renewables, Algerian LNG, and Azerbaijani natural gas via the Trans Adriatic Pipeline.

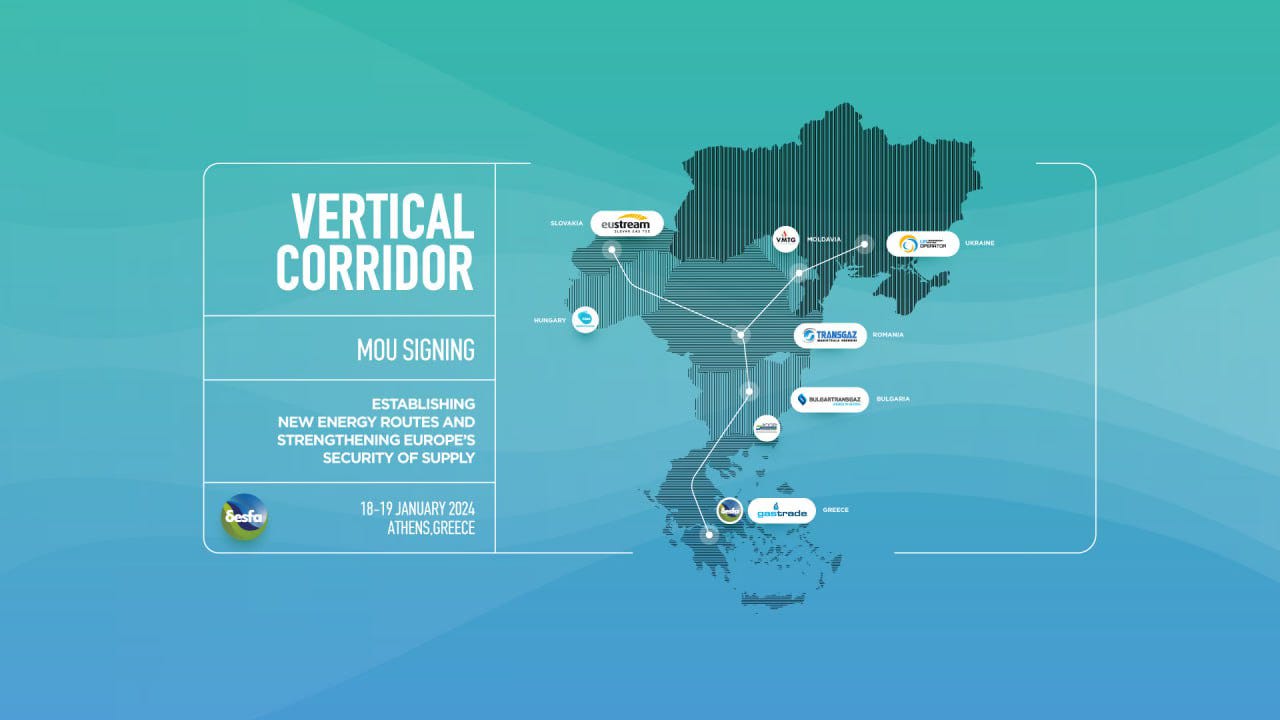

The true catalyst for Greece's current hub ambitions came with the historic price shocks of 2022. Sensing a unique geopolitical opening, Athens began directing substantial capital, backed by the European Union’s post-pandemic recovery fund, into major infrastructure projects. The centerpiece of this strategy is the vertical gas corridor, a south-to-north transit route designed to connect Greece’s maritime grid to consumers in Central Europe and Eastern Europe, extending all the way to Ukraine, which Greece actually began supplying last December.

This expansion is framed as a regional triumph, yet its operational blueprint is heavily guided by external interests; the United States Energy Association (USEA) has positioned itself as the central convener for the project, signing Memoranda of Understanding with 11 regional gas transmission system operators to direct technical and policy dialogue.

For years, the vertical gas corridor attracted little more than polite indifference from commercial players, crippled by regulatory constraints on long-term capacity bookings and severe pipeline bottlenecks. But with the looming 2027 deadline for the total elimination of Russian gas, the corridor has suddenly gained commercial traction. Buyers are now scrambling for long-term security, reportedly reserving loading slots at Greece’s Revithoussa import terminal all the way through to 2040.

This domestic expansion has predictably caught the attention of Washington, which views Greece as a convenient geopolitical instrument to penetrate markets in Central and Eastern Europe where American gas has traditionally struggled to compete. By 2025, more than 80% of Greece’s LNG imports originated from the United States.

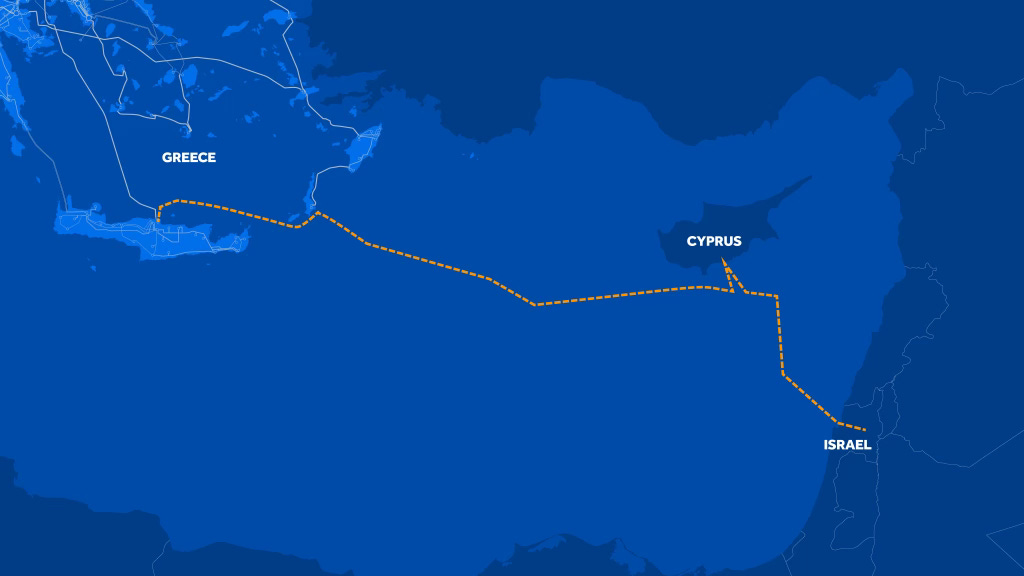

To solidify this relationship, Washington and Athens signed a 20-year agreement last November, committing the United States to supply approximately 15 billion cubic meters of LNG over the lifespan of the contract. Concurrently, the United States is leveraging Greece to project power in the volatile Eastern Mediterranean. Washington has thrown its diplomatic weight behind the 3+1 energy partnership, linking Greece, Cyprus, and Israel in an effort to develop offshore gas reserves and connect regional power grids through the proposed 2 billion euro Great Sea Interconnector.

While Washington provides much of the geopolitical backing and diplomatic pressure behind the initiative, it is the European Commission that has largely been left to bankroll the project, allocating €657 million in taxpayer funding. Meanwhile, the estimated cost of the interconnector has ballooned from its original €1.2 billion budget to roughly €1.9 billion. This sharp escalation has triggered a bitter regulatory standoff between Athens and Nicosia over cost-sharing mechanisms and the eventual financial burden imposed on domestic consumers.

American energy conglomerates have wasted no time capitalising on this state-sanctioned access. ExxonMobil signed exploration agreements for an offshore block in western Greece last November, and more recently, a consortium led by Chevron secured exclusive rights to hunt for natural gas off the southern Greek coast. For the Greek government, which has spent years aggressively deepening its diplomatic and military ties with the United States, this corporate influx is celebrated as a profound validation of the transatlantic alliance.

Yet, looking at this development through a wider lens reveals that Greece’s supposed triumph may actually be a strategic trap for Europe. By locking itself into binding, decades-long LNG contracts, the European Union is actively sabotaging its own green deal goals and making a mockery of its climate commitments.

More fundamentally, this strategy does not achieve energy autonomy; it merely swaps a hostile dependency for a highly unpredictable one. Europe is trading its historic submission to Russian pipelines for a total reliance on American shipping lanes. While Washington is a democratic ally, it is no longer a guaranteed partner. Decades of deepening friction, amplified by Donald Trump’s ongoing hostility toward NATO and the European continent, have proven that American foreign policy can shift overnight. By anchoring its entire grid to Washington’s political whims, Europe risks finding itself stranded with exorbitant energy bills the moment domestic American priorities change

Greece may very well succeed in building its regional energy hub, but its ultimate survival will depend entirely on how skilfully Brussels can navigate an increasingly asymmetric and volatile relationship with the United States.

Subscribe to receive my posts directly in your inbox and support my work!

Share this with anyone if you think their attention span can survive more than two paragraphs — and if not, send it anyway. 📨

Great article. And the EU — the home of Machiavelli and von Clausewitz — forgot an eternal rule: you are either independent or you are not. And if you are dependent, whom you are dependent on is of lesser consequence - be it Russia or LNG supplied by the US. You are not independent, and that has real costs associated. For example, the Japanese in the 1980s would have never signed the economically devastating Plaza Accord with the US, had they not been dependent on the US. And one can argue that the Japanese economy never quite recovered. Dependency is a sweet poison. Europe would do well to remember that before locking itself into another half-century of dependency.

Thank you once again for an excellent piece!

European leaders seem to have learnt nothing from the 2022 Russian fiasco, and the US (despite the narrative all being about the power vacuums it seems to be leaving as an aftermath of this administration’s decisions) on the other side continues to capitalize on strategic decisions.

Having the EU pay for the infrastructure that will allow US companies to make $$$ is having your cake and eating it!

Curious to see how this evolves in the medium and long term. Keep at it, Atlas!