Trojan Horse

Russia turned critical molecules into Europe’s next strategic trap

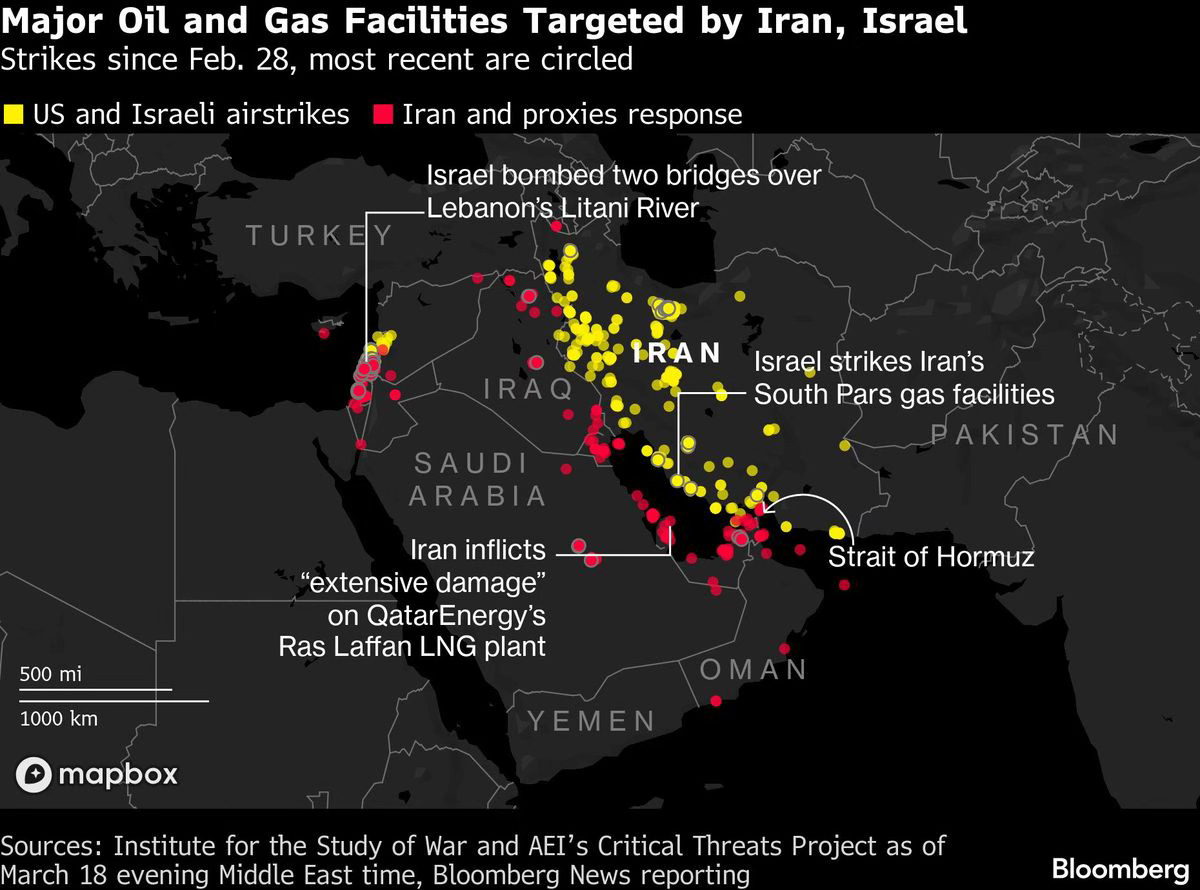

While global powers have their eyes fixed on the kinetic exchanges in the Middle East, a shift in global supply chains is occurring in the background that threatens to concrete Europe’s geopolitical architecture for decades to come.

The escalation between Iran, Israel and the United States has sent energy markets into a state of high alert, but to view this through the lens of oil prices alone is to miss the structural rot beneath the surface. When these powers target each other’s energy assets, we are not just discussing oil prices; we are discussing the very molecules that sustain the global population. The recent targeting of Middle East energy infrastructure has caused oil and gas prices to jump, but the real blow to the West is the invisible strangulation of the European fertilizer industry.

The reality of fertilizer production is that it is essentially solidified natural gas. Natural gas serves not only as the primary energy source but also provides the hydrogen necessary to bind nitrogen from the air into ammonia. This process is punishingly energy-intensive, with natural gas accounting for 80% to 90% of the variable costs.

The vulnerability of this chain was laid bare when Chevron declared force majeure and shut down the Leviathan gas field in Israel. Leviathan is a vital artery for Egypt, which relies on that gas to power its own industry. Since Egypt is one of the world's largest exporters of fertilizer, a hiccup in an Israeli gas field quickly manifests as a supply shock in the global ammonia market.

This fragility is not an outlier, it is the new baseline. When supply lines in the Middle East come under pressure, the precarious global balance collapses. The situation reached a critical point when Oman closed its ports, effectively cutting off the last ammonia export route from the Middle East. With major production plants in Iran—a country that has invested billions to become a regional fertilizer hub—going offline or becoming inaccessible, a crucial supply artery for the world has been cauterized.

For a continent like Europe, already struggling with the de-industrialization of its chemical sector, this is not a temporary inconvenience. It is an existential crisis.

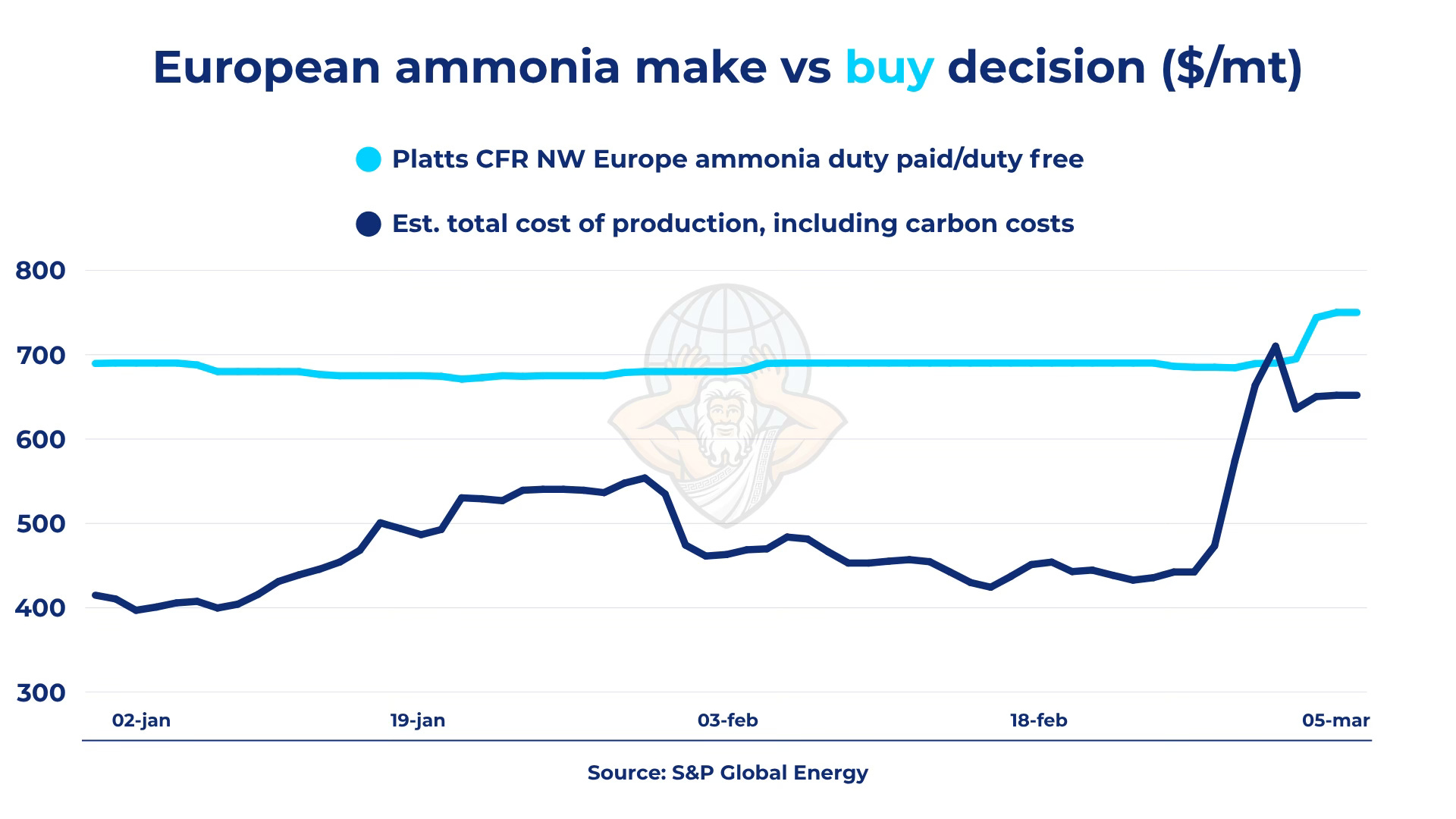

Predictably, as the physical supply of energy tightens, the economic logic in Europe has become utterly absurd. Driven by exploding gas prices, European ammonia import prices recently reached a three-year high of over $750 per metric ton. The cost of domestic production rose so sharply—at times costing $150 to $200 more per ton to produce locally than to import—that European industrial giants were forced to shutter plants. This is the definition of a strategic death spiral: domestic production capacity is wiped out by unsustainable marginal costs, which only deepens the reliance on foreign actors.

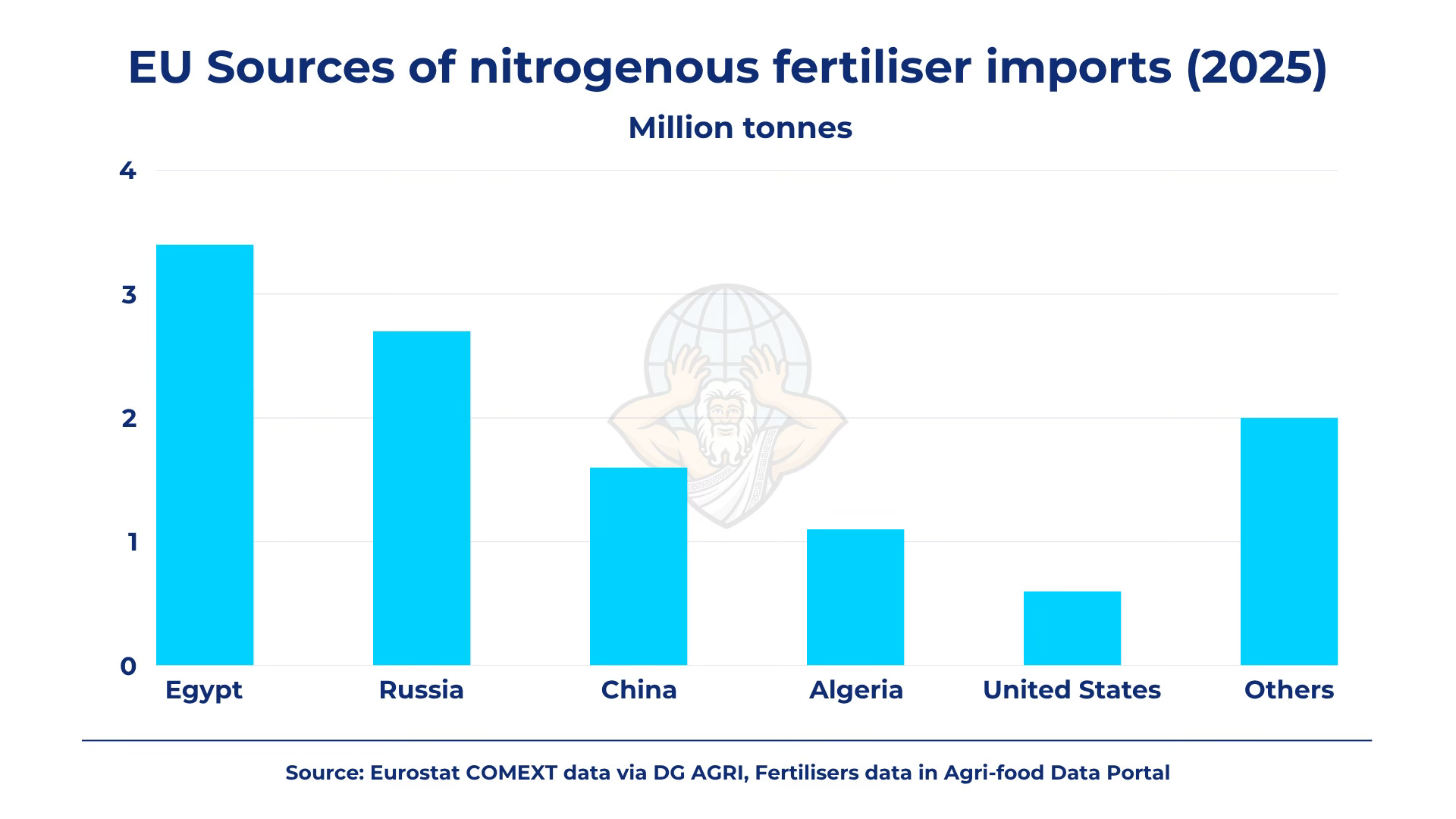

Into this vacuum steps a player who knows exactly how to monetize this uncertainty. While Europe de-industrializes itself in a bid for moral purity, Russia is consolidating its position as the indispensable granary of the world. Moscow now accounts for roughly 26% of EU fertilizer imports, a statistic that reveals a profound strategic failure.

For the Kremlin, fertilizer is the perfect geopolitical Trojan horse. It is a way to export natural gas by proxy, effectively evading sanctions targeted at raw energy flows. By converting its vast gas reserves into value-added chemicals, Russia bypasses the restrictions that plague its pipeline business. It is a masterful move; while the EU debates gas price caps, it remains wide open to "processed gas" arriving in the form of urea and nitrates.

The numbers tell a story of resilience that Western policymakers chose to ignore. After the Ukraine invasion, Russia’s fertilizer export revenues surged, rising about 70% in just a few months. All despite expectations that sanctions would reduce them. Europe replaced lost gas with U.S. LNG, while Russia redirected its gas into fertilizer production, where gas accounts for roughly 70–80% of costs.

Europe is swapping energy dependence on Russia for reliance on fertilizers—critical not only for food production, but also for the defense sector, where nitrogen-based inputs such as ammonia are used in explosives and propellants. And predictably, Europe still sources a large share of it from Russia.

Beyond Russia, Egypt is also a major supplier. But it is hardly a reliable one, as its fertilizer production remains highly vulnerable to geopolitical disruptions across the Middle East. Last year, during Trump’s 12-day standoff with Iran, Egyptian fertilizer plants were forced to halt operations after natural gas imports from Israel—mainly from the Leviathan gas field—fell sharply. The current war with Iran is producing a similar outcome: Egypt’s largest fertilizer producers, including Abu Qir Fertilizers and MOPCO, are reportedly operating at only around 60–70% of capacity.

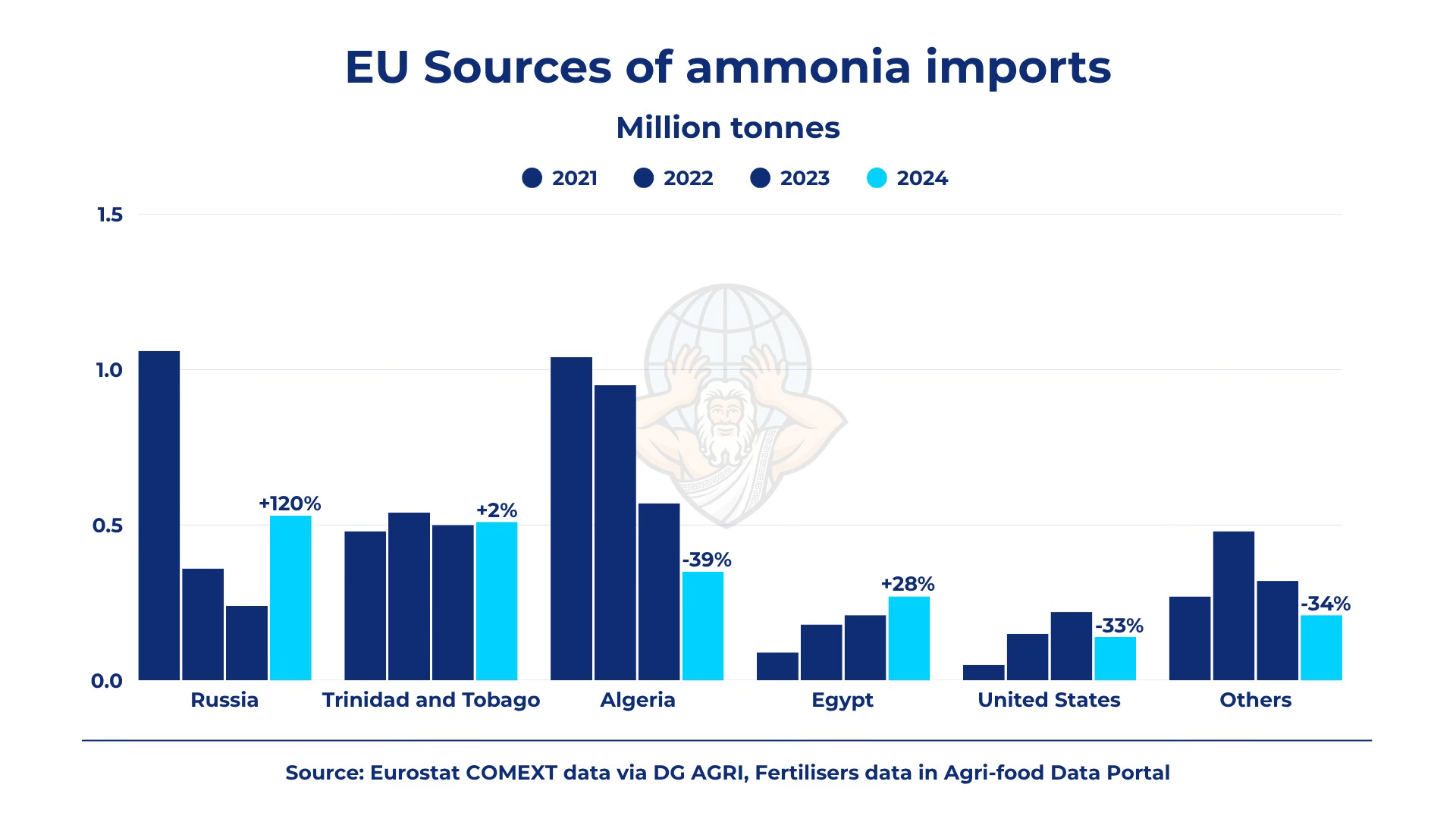

After Russia’s invasion of Ukraine in 2022, EU ammonia imports from Russia initially fell—as one would expect from a bloc supposedly trying to reduce strategic dependence. But by 2024, Russian volumes had surged back by 120% compared to the year before, while imports from most alternative suppliers barely grew or outright declined.

This matters because ammonia is not just another commodity; it is the backbone of nitrogen fertilizers and, by extension, modern food systems, explosives, and propellants. At a moment when Europe is scrambling to meet NATO defense targets and rearm at speed, dependence on a strategic rival for such a foundational chemical is more than uncomfortable, it is structurally reckless. You do not want to build your deterrent around a supplier that could restrict the flow of essential inputs overnight.

And that is not a theoretical risk, it happened last week. According to a government statement, Moscow temporarily suspended ammonium nitrate exports. A useful reminder that Russia can tighten this market almost overnight if it chooses to.

One would think Europe had learned something from the fertilizer crunch of 2022—or, more broadly, from the risks of depending on its geopolitical adversaries. Evidently, it has not.

In this environment, more sanctions on Russian fertilizers are unlikely to achieve anything. Russia will almost certainly find workarounds, as it has elsewhere. Andrei Guryev, head of the Russian Fertilizer Producers Association (RAFP), is hardly pretending otherwise:

“We are not afraid of any duties or tariffs. The market is large. The main thing is that we are moving specifically to the BRICS countries’ market.

Today, the BRICS market accounts for almost 50% of all mineral fertilizer consumption, and it is a market that will continue to grow.”

More importantly, the global system cannot absorb the shock of a total rupture. Britain’s food and drink industry is already warning that food prices could rise by nearly 10% by year-end as a result of the Iran war, roughly triple its earlier forecast. Against that backdrop, disrupting Russian fertilizer flows would look less like strategy and more like self-harm.

Moscow understands this. Fertilizers are no longer just an input for agriculture. They now sit at the crossroads of food security, industrial resilience, and strategic leverage.

Russia already accounts for roughly 15% of global fertilizer exports, but Moscow is aiming higher. In a recent meeting with Putin, Andrei Guryev said the industry is targeting a 25% share of the global market by 2030. That is not a trivial ambition, it reflects a clear understanding of the geopolitical leverage that comes with controlling such a foundational market.

For Europe, that would harden an already uncomfortable dependency. Even as Russia remains cut off from much of the Western financial system and politically estranged from Europe, it still matters where it counts most: in the supply of essential physical commodities.

Ultimately, what Moscow is exporting is not just fertilizer, but a permanent state of dependence embedded deep within the modern economy.

Subscribe to receive my posts directly in your inbox and support my work!

Share this with anyone if you think their attention span can survive more than two paragraphs — and if not, send it anyway. 📨

Thank you for putting this together! Very valuable and sobering commentary that a lot of people seem to miss

Great analysis - thanks for sharing it.